This Week in SaaS - April 28 - May 4, 2026

The top M&A deals, venture deals, news, and blog posts of the week

📚 New Blog Posts

- The Agentic Engineering Trends Report 2026

- How to Transform Your Engineering Team with Agentic Engineering

- CEO Mastermind Recaps for the Week of April 27 - 30, 2026

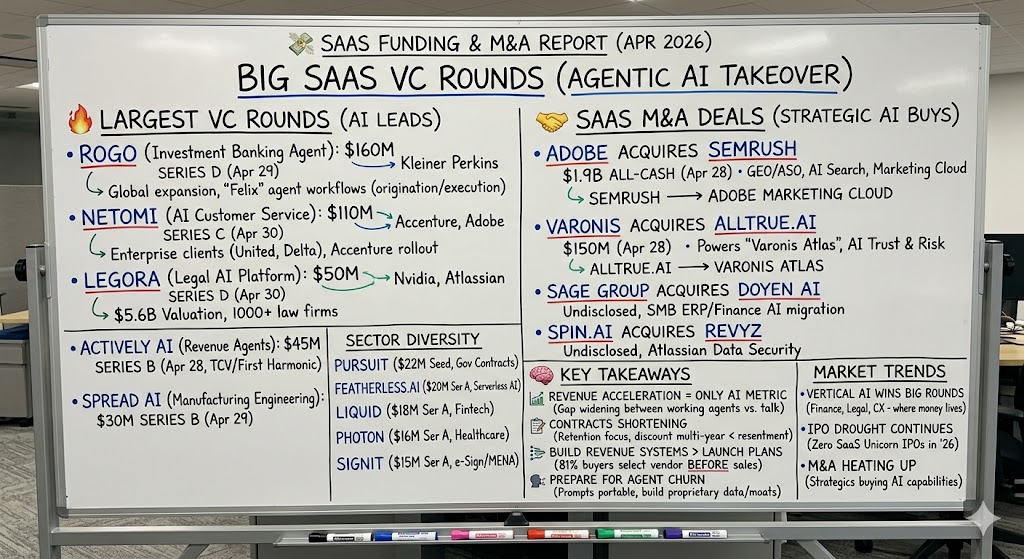

💸 Big SaaS VC Rounds

- Rogo (agentic AI platform for investment banking and financial services; SaaS) – raised a $160M Series D on April 29, 2026, led by Kleiner Perkins with participation from Sequoia, Thrive Capital, Khosla Ventures, J.P. Morgan Growth Equity Partners, BoxGroup, and Jack Altman; funds will accelerate global expansion, deepen partnerships with leading financial institutions, and scale Rogo's "Felix" agent across origination, execution, advisory, and portfolio intelligence workflows.

- Netomi (agentic AI customer service platform; SaaS) – raised a $110M Series C on April 30, 2026, led by Accenture Ventures, with participation from Adobe Ventures, WndrCo, Metis Strategy, NAVER Ventures, and Fin Capital; funds will support customer deployments and R&D, with Accenture training hundreds of employees to roll out the platform to enterprise clients including United Airlines, Delta, Paramount, and DraftKings.

- Legora (collaborative AI platform for legal work; SaaS) – raised a $50M Series D extension on April 30, 2026, with new backing from Atlassian and Nvidia's NVentures (Nvidia's first legal-tech investment); funds will scale the platform — already used by 1,000+ law firms across 50+ markets — at a $5.6B post-money valuation as the company crosses $100M ARR.

- Actively AI (intelligence-led revenue platform with persistent per-account AI agents; SaaS) – raised a $45M Series B on April 28, 2026, co-led by TCV and First Harmonic with participation from Bain Capital Ventures, First Round Capital, and Alkeon; funds will expand product, hire GTM talent, open a new San Francisco office, and scale deployments at customers including Samsara, Ramp, Ironclad, and Attentive.

- SPREAD AI (Berlin-based AI engineering intelligence platform for manufacturers; SaaS) – raised a $30M Series B on April 29, 2026, with new investors DTCP Growth, IQT, OTB Ventures, Salesforce Ventures, and Thesiger Capital alongside HV Capital and Nauta Capital; funds will support international expansion, advanced AI agents, and deeper product-data capabilities for automotive, aerospace, and industrial-equipment customers (incl. Volkswagen, BMW, Rheinmetall).

- Pursuit (AI-powered platform that helps companies win government contracts; SaaS) – raised a $22M seed round on April 29, 2026, led by OpenGov co-founder Mike Rosengarten at Builders VC, with participation from Bill Gurley, Jack Altman, and Sam Hinkie at 87 Capital; funds will expand AI-driven scanning of public data across ~11,000 state, local, and education entities, surfacing budgets, contracts, and RFPs.

- Featherless.ai (serverless inference platform for open-source AI models; SaaS) – raised a $20M Series A on April 30, 2026, co-led by AMD Ventures and Airbus Ventures, with participation from BMW i Ventures, Kickstart Ventures, Panache Ventures, and Wavemaker Ventures; funds will expand global infrastructure and launch a marketplace for specialized open models.

- Liquid (leveraged trading platform; fintech SaaS) – raised an $18M Series A on April 30, 2026; funds will expand product capabilities and trading infrastructure for the platform's growing user base.

- Photon (prescription access platform; healthcare SaaS) – raised a $16M Series A on April 30, 2026, led by Healthier Capital, with participation from Notation, Flare Capital, and Evidenced; funds will expand prescription routing and pharmacy access infrastructure for healthcare partners.

- Signit (Saudi Arabia–based digital signature and AI-powered contract management; SaaS) – raised a $15M Series A on April 28, 2026; funds will expand the digital trust and contract automation platform across MENA enterprise customers.

🤝 SaaS M&A Deals

- Adobe completed the acquisition of Semrush (~$1.9B all-cash; brand visibility, SEO, and AI-search optimization SaaS, US) – completion announced April 28, 2026; the acquisition expands Adobe's marketing cloud with capabilities across SEO, generative engine optimization (GEO), and agentic search optimization (ASO) as enterprises adapt to AI-driven discovery.

- Varonis Systems completed the acquisition of AllTrue.ai (~$150M reported; AI trust, risk, and security management SaaS, US) – disclosed alongside Q1 2026 results on April 28, 2026; AllTrue.ai powers the newly launched Varonis Atlas product, providing visibility, control, and real-time guardrails for AI systems and agents across the enterprise.

- Sage Group completed the acquisition of Doyen AI (terms undisclosed; AI-driven onboarding/data-migration SaaS for finance teams, UK/US) – announced April 28, 2026; the acquisition strengthens Sage's AI strategy by accelerating customer migrations from legacy systems and improving go-live speed for SMB ERP and finance deployments.

- Spin.AI completed the acquisition of Revyz (terms undisclosed; SaaS data resiliency and security posture management for Atlassian Jira/Confluence, US) – announced April 28, 2026; the acquisition extends Spin.AI's data protection platform into the Atlassian ecosystem, unifying backup, security, and configuration management across enterprise SaaS stacks.

🧠 Key Takeaways

- Revenue acceleration is the only AI metric that matters. SaaStr's late-April mashup with TBPN argues that "AI talk is cheap" and that founders, CROs, and CMOs in 2026 fall into two camps: those who can deploy a working AI agent by Friday and those who can't — and the gap widens weekly.

- Contracts are getting shorter — design retention around it. Sub-1-year deals have grown from 4% in 2023 to 13% in 2026 while three-year deals dropped from 28% to 23%; SaaStr advises that discounting for multi-year commitments creates customers who resent the lock-in by month 18, and recommends compensating reps on net new recurring revenue rather than total contract value.

- Build a revenue system, not a launch plan. A late-April Effiqs analysis outlines five structural GTM decisions (positioning architecture, hybrid PLG/SLG motion, lifecycle programs, revenue intelligence, and attribution) that determine whether B2B SaaS pipeline compounds or plateaus — citing that 81% of buyers now select a vendor before ever speaking to sales.

- Prepare for AI-agent churn — prompts are portable. SaaStr warns that buyers of AI agents are explicitly refusing multi-year commitments because switching costs are low and prompts are portable; 75–85% gross retention is plausible for vendors that don't build stickiness beyond the model itself, making proprietary data, workflow embedding, and outcomes contracts the new moats.

- Vertical AI is where 9-figure rounds are landing. This week's biggest SaaS rounds (Rogo for finance, Legora for legal, Netomi for CX, Actively for revenue ops) reinforce a16z's thesis that the AI opportunity now lives in legacy verticals outside Silicon Valley, where forward-deployed founders amplify customer economics rather than just automating tasks

- The SaaS IPO drought continues — but M&A is heating up. Crunchbase News' April 27 analysis notes zero new venture-backed SaaS unicorn IPO filings so far in 2026, while strategic acquirers (Adobe/Semrush, Varonis/AllTrue, Sage/Doyen, Spin.AI/Revyz all closing on April 28 alone) are aggressively buying for AI capabilities. Founders weighing exits should watch the strategic-buyer market more closely than the IPO calendar this year.

📰 Community News

- Apply to join the SaasRise community for SaaS CEOs and Founders with $1M+ in ARR

- Apply to join the GrowthRise community for B2B Marketing Leaders

- Join Pulse, our AI-curated tech news reader, to see the latest SaaS, AI, and tech news and deals

See you next week with the next edition ofThis Week in SaaS.

-Ryan Allis, CEO of SaasRise