Secondary Markets & Founder Liquidity in SaaS and AI

If you’re a SaaS or AI CEO with $5M–$100M+ in ARR, you’ve probably had this thought: “I’ve built something worth $50M… $100M… maybe more. But I can’t access any of it.”

You’re not alone. Most software founders have nearly their entire net worth locked inside a single, illiquid company. The good news: a maturing secondary market—now $233 billion in annual volume—means you no longer have to sell your entire company or wait for an IPO to turn that paper wealth into real wealth. This report is your complete guide to founder liquidity in 2026: the four structures available to you, the multiples you can expect, 50 real-world examples with disclosed terms, and a step-by-step playbook for taking $5M–$100M+ off the table while keeping majority control.

This report is published by SaasRise, the #1 mastermind community for experienced SaaS CEOs with $1M–$100M+ in ARR. Members have collectively raised $1B+ and have $3B+ in ARR.

🎯 Who This Report Is For:

• SaaS founders and CEOs with $5M–$100M+ ARR who want to take money off the table without selling the company

• AI-native software founders experiencing rapid growth who need to understand their liquidity options

• CFOs and founding teams preparing for a minority recap, tender offer, or secondary share sale

• Any software founder who wants to understand what their company is worth on the secondary market—and how to maximize it

📋 Table of Contents

- Executive Summary

- 34 Real Examples of SaaS Founder Liquidity Rounds

- AI-Native Software: The New Wave of Founder Liquidity

- Case Study: Ryan Allis & iContact

- The State of the Secondary Market in 2025–2026

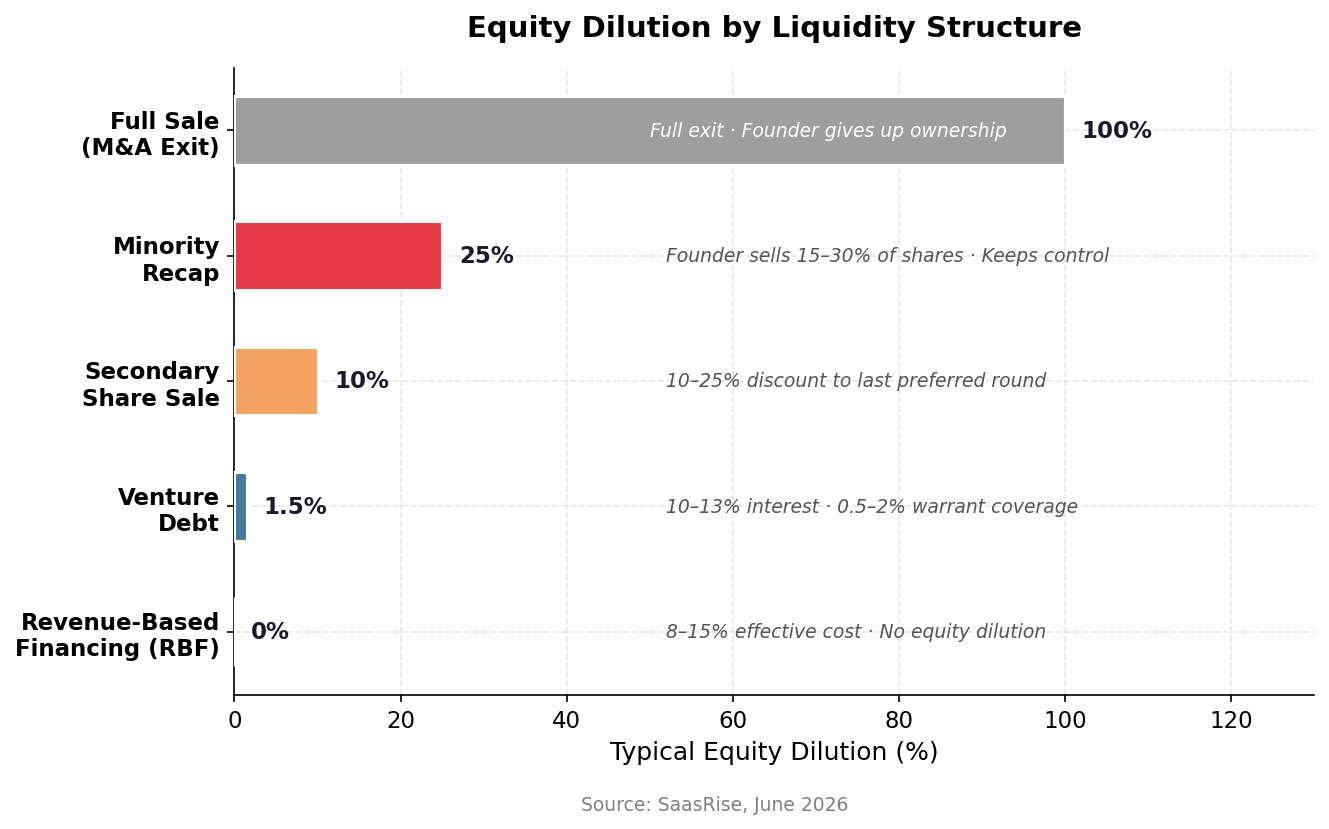

- Understanding Founder Liquidity Structures

- Valuation Multiples in Secondary & Recap Rounds

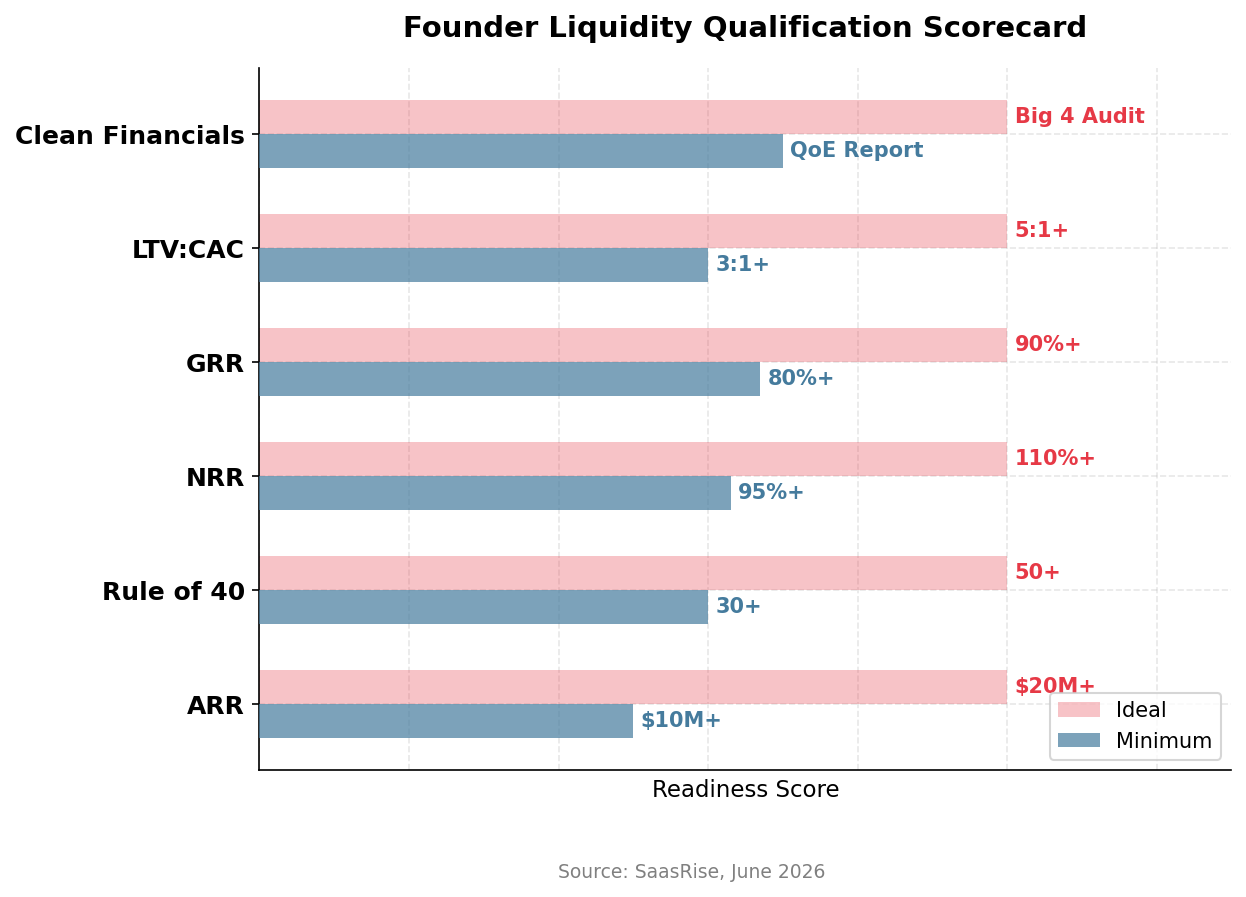

- What Investors Look For: Qualifying for Founder Liquidity

- How to Maximize Your Valuation Multiple

- The Minority Recap Playbook — Step by Step

- Tender Offers: The New Liquidity Playbook

- GP-Led Continuation Vehicles: A New Path for SaaS

- Venture Debt, Revenue-Based Financing & Non-Dilutive Alternatives

- The Psychology of Founder Liquidity

- Looking Ahead: 2026–2027 Outlook

- What to Do With Your Liquidity: A Founder’s Financial Playbook

- Conclusion & How SaasRise Can Help

1. Executive Summary

Here’s the bottom line: you do not have to sell your company to create life-changing wealth.

The secondary market for private company shares hit an all-time record of $233 billion in 2025—up 53% year-over-year. Tender offers, minority recaps, and structured secondary sales have become mainstream tools that SaaS and AI founders are using right now to take $5M–$100M+ off the table while keeping majority control. Five years ago, most of these options didn’t exist at scale. Today, they’re the playbook.

In this report, you’ll find everything you need to evaluate and pursue founder liquidity:

- Four liquidity structures explained in plain language—which one is right for your situation

- 50 real-world examples of SaaS and AI-native companies that took secondary liquidity, with disclosed valuations and multiples

- A step-by-step minority recap playbook—what to do month-by-month, who to hire, what to watch out for, and common mistakes to avoid

- The metrics that matter—what investors actually look for, and how to maximize your valuation multiple before going to market

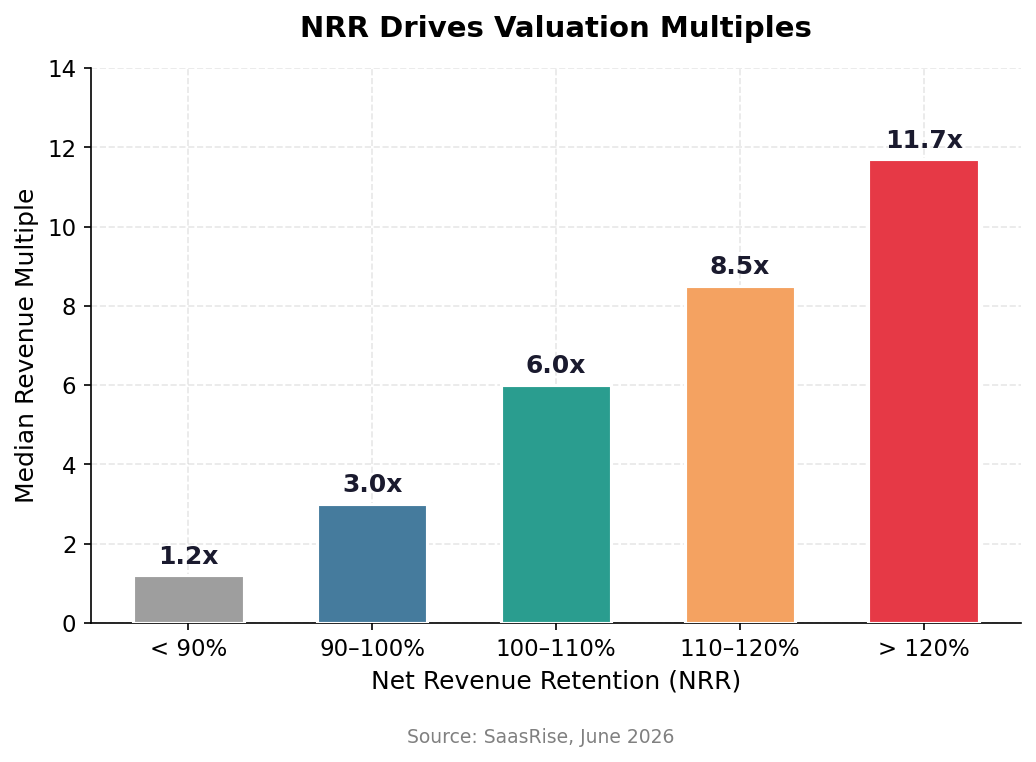

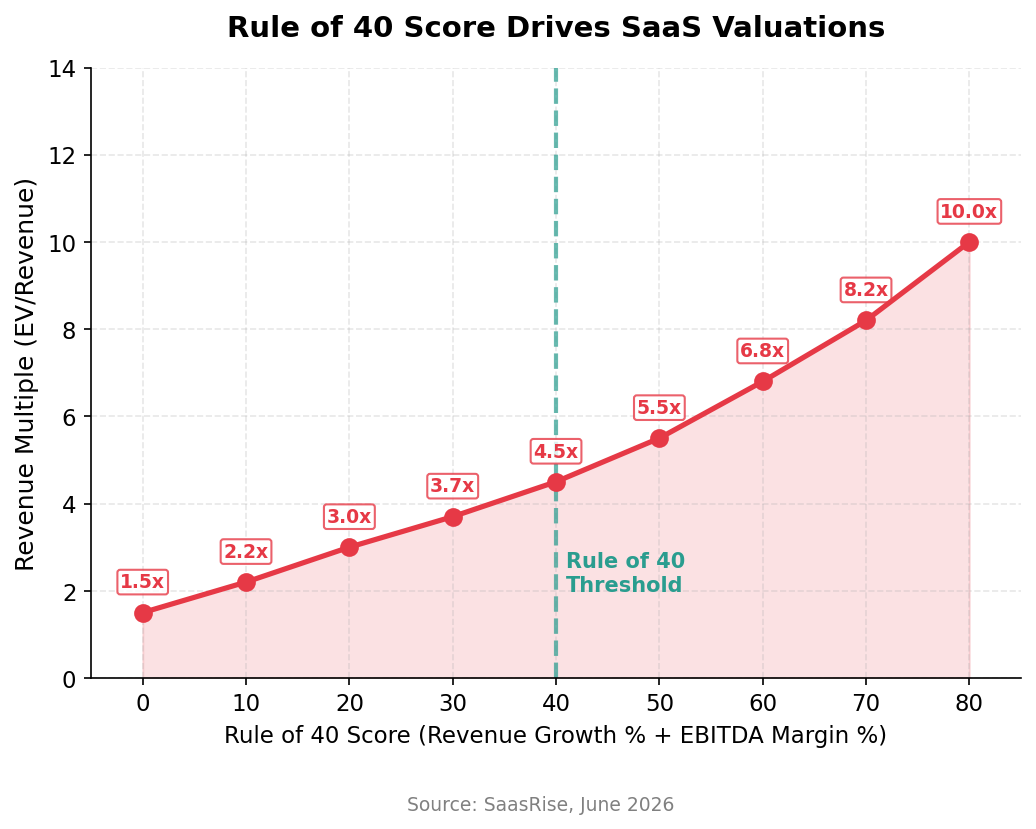

The core thesis is straightforward: with the right metrics (Rule of 40+, $10M+ ARR, strong net revenue retention), the right advisors, and the right structure, you can take millions off the table while retaining majority ownership and positioning for a much larger exit down the road.

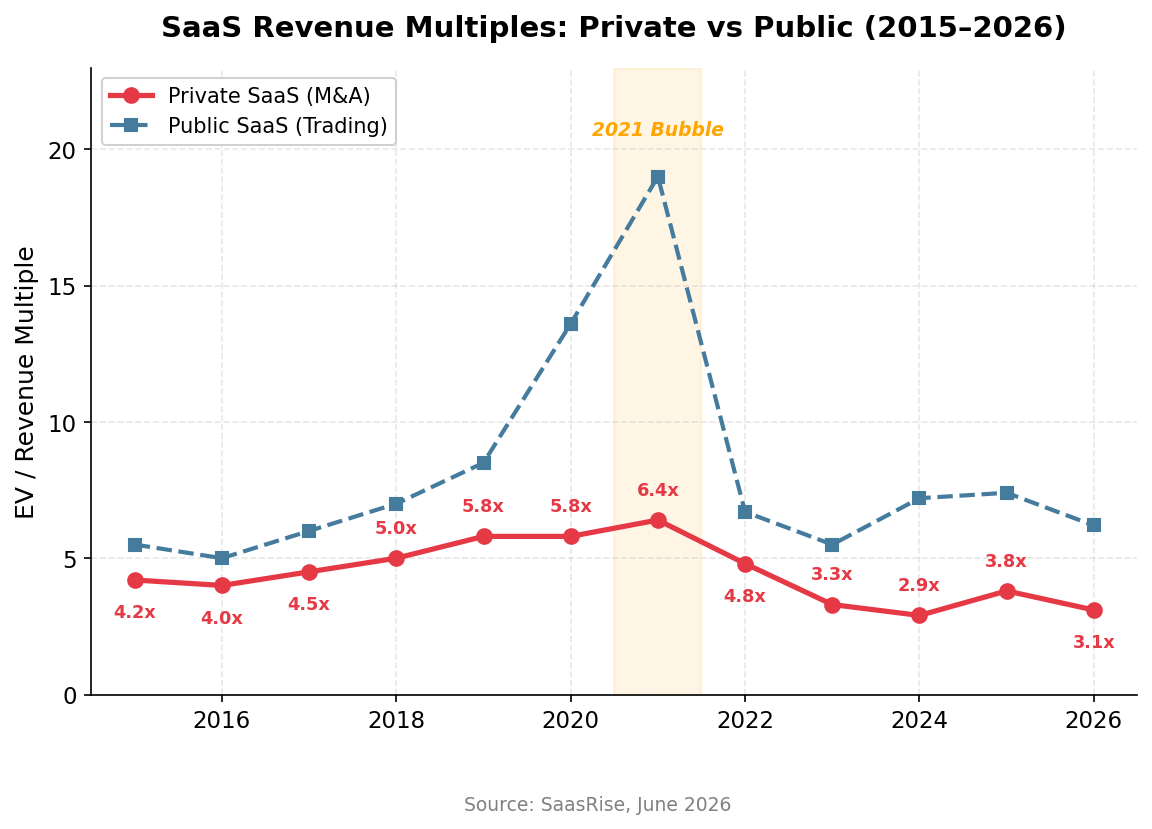

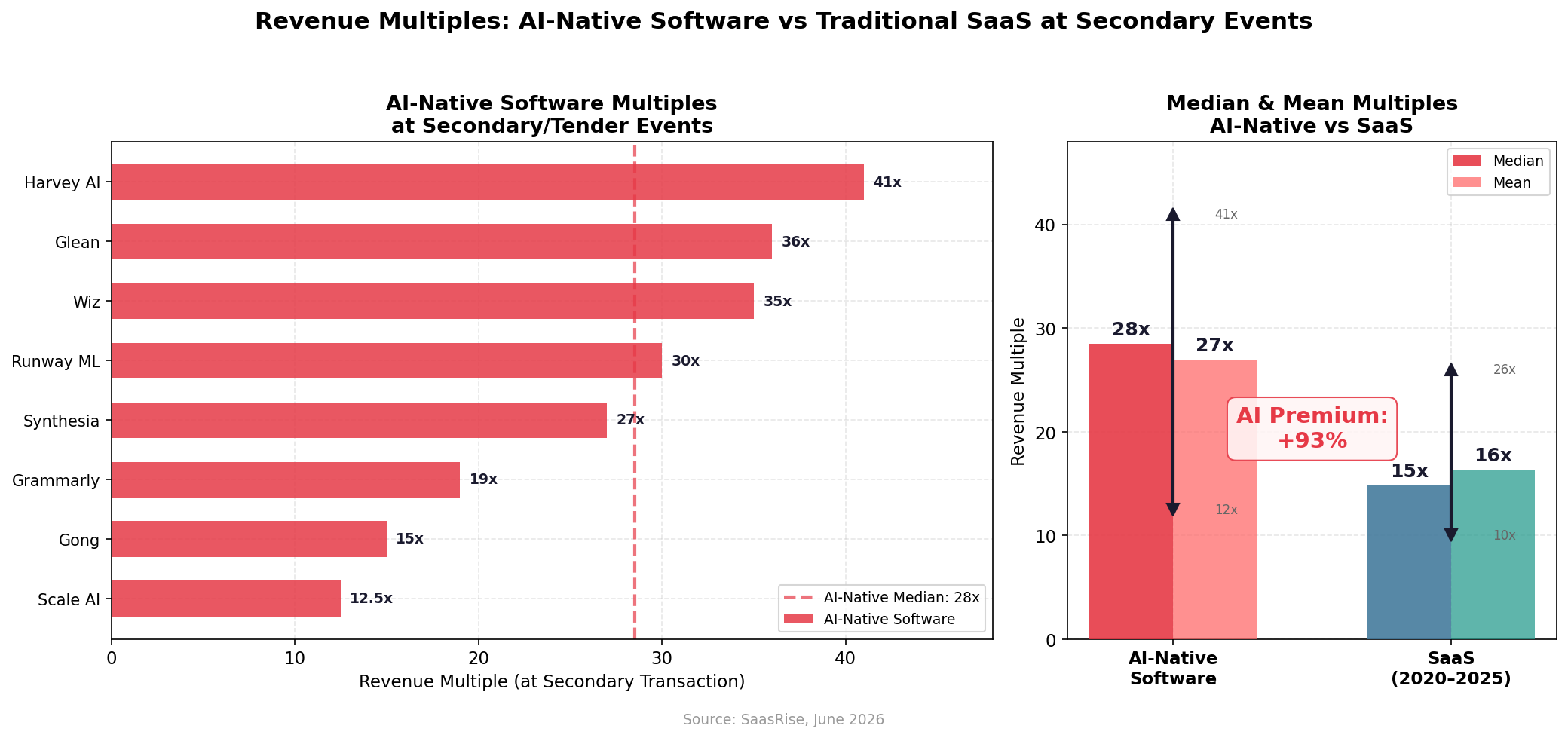

Notably, AI-native software companies are commanding a significant valuation premium in secondary transactions. Where traditional SaaS deals in 2020–2025 settled at a median of ~15x revenue, AI-native companies are transacting at a median of ~28x—a +93% premium. Consider: Harvey AI’s December 2025 tender offer valued the company at ~41x revenue on ~$195M ARR, while Glean’s secondary shares traded at ~36x on ~$200M ARR. By contrast, even strong SaaS transactions like Notion’s $270M tender at $11B (~18x on ~$600M ARR) and Databricks’ $62B round (~21x on ~$3B ARR) came in well below the AI-native median. The takeaway: if you are building AI-native software, the liquidity window is not just open—it is extraordinarily favorable.

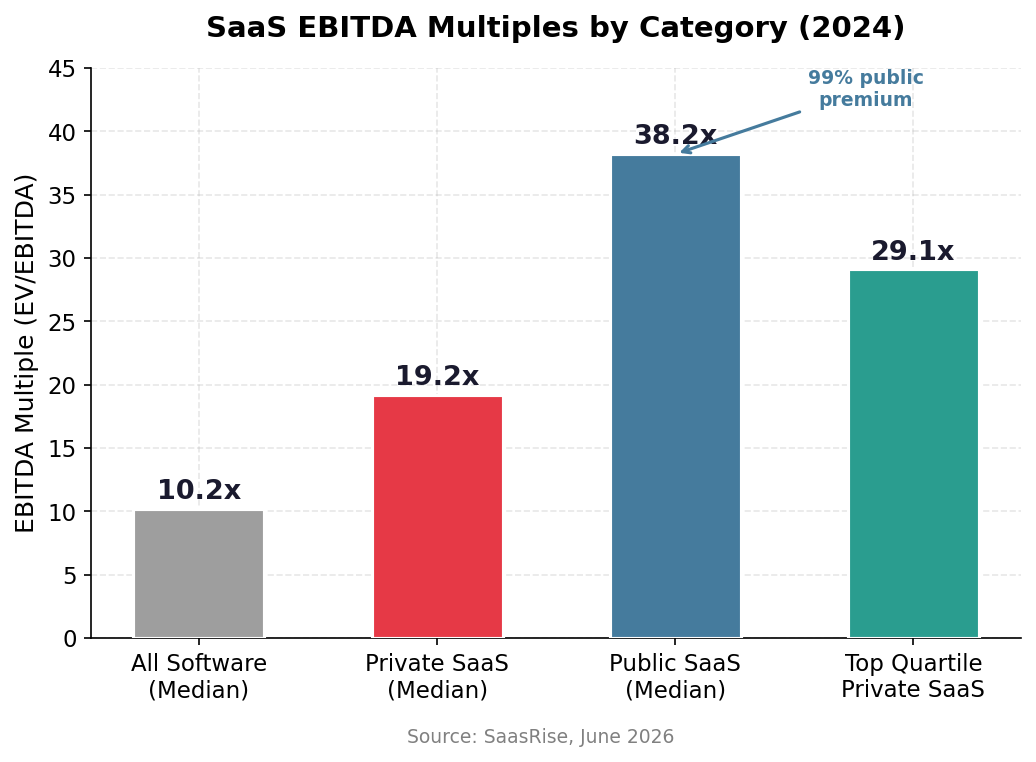

Key Takeaway: The median private SaaS revenue multiple in 2024 was 4.1x, with the median EBITDA multiple at 19.2x. AI-native software companies command a ~28x median multiple at secondary events—nearly 2x the SaaS median of ~15x. Founders who hit Rule of 40+ with $10M+ ARR can realistically access secondary liquidity of $5M–$100M+ while keeping majority ownership and control.

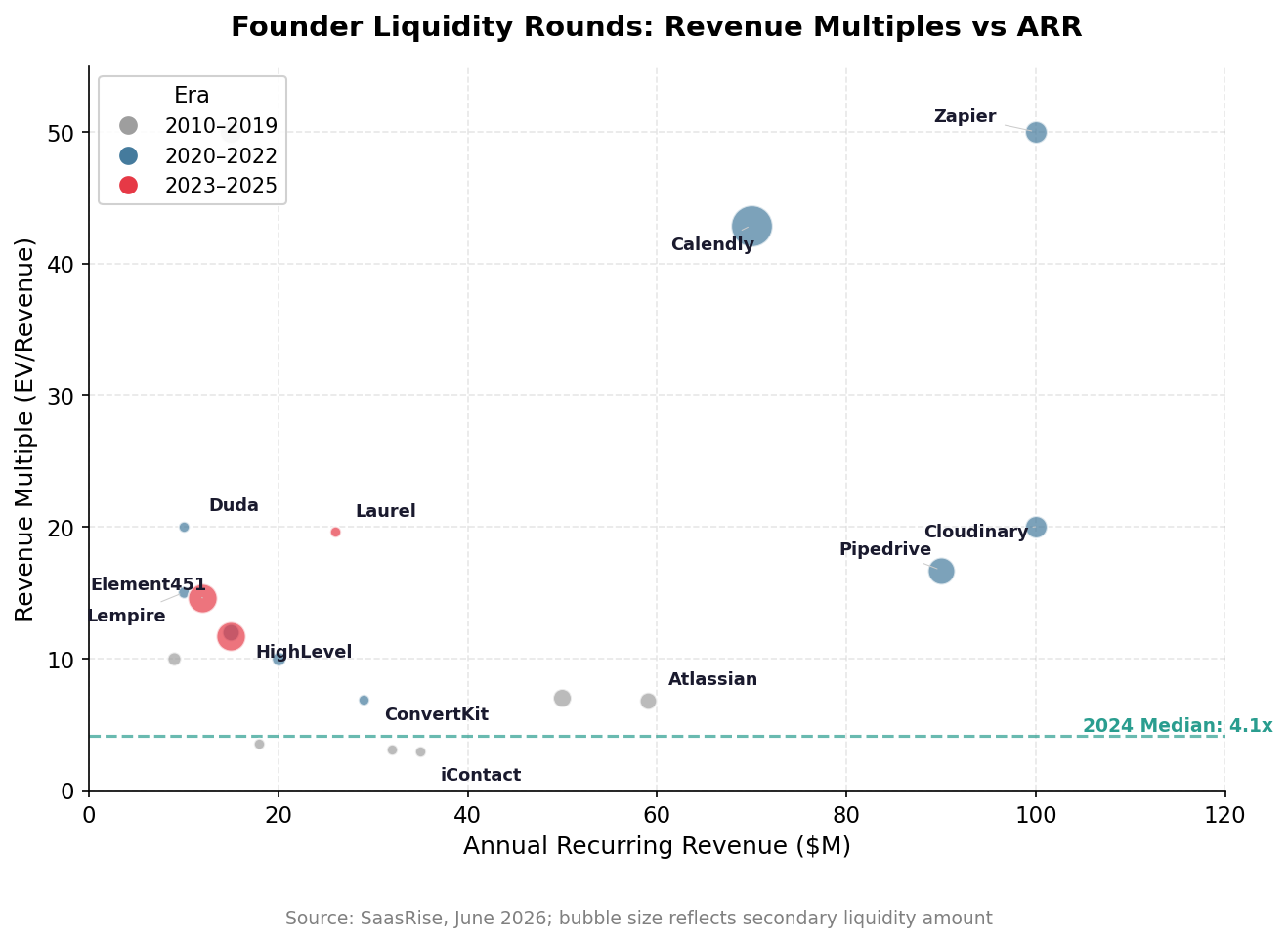

2. 34 Real Examples of SaaS Founder Liquidity Rounds

Nothing makes the opportunity more real than seeing what other founders have actually done. The following tables compile 34 documented founder liquidity transactions in SaaS and tech, spanning from 2010 to 2025—including minority recaps, secondary share sales, and structured tender offers. Study them carefully. The founder who did a $15M recap at $35M ARR (iContact) and the one who did a $350M secondary at $70M ARR (Calendly) were in fundamentally different market conditions—but both accessed life-changing liquidity without selling their companies.

2020–2025 Era Transactions

| Company | Date | Secondary Liquidity | Valuation | ARR (Est.) | Rev. Multiple | Type |

|---|---|---|---|---|---|---|

| Notion | Dec 2025 | $270M | $11B | ~$600M | ~18x | Employee tender offer |

| Gusto | Jun 2025 | $200M+ | $9.3B | ~$750M | ~12x | Employee tender offer |

| Laurel (Time by Ping) | Jun 2025 | $20M | $510M | $26M | 19.6x | Secondary round |

| Ramp | Mar 2025 | $150M | $13B | ~$500M | ~26x | Employee secondary |

| ROKT | Jan 2025 | $335M | $3.5B | Undisclosed | — | Secondary share sale |

| Databricks | Dec 2024 | ~$10B (incl. secondary) | $62B | ~$3B | ~21x | Primary + employee tender |

| Element451 | Dec 2024 | $175M | ~$175M | ~$12M | 14.6x | Minority recap |

| Wrapbook | Sep 2024 | $20M | Undisclosed | Undisclosed | — | Secondary round |

| Clio | Jul 2024 | Substantial (in $900M round) | $3B | ~$200M | 15x | Secondary in Series F |

| Figma | May 2024 | $600–900M | $12.5B | ~$600M | ~21x | Shareholder tender offer |

| Canva | Feb 2024 | ~$1B+ | $26B | ~$2B | ~13x | Employee + investor stock sale |

| Hostaway | May 2023 | $175M | ~$175M (est.) | ~$15M | ~12x | Growth round |

| Deel | Feb 2023 | $300M | $12B | ~$200M | ~60x | Secondary + tender |

| Cloudinary | Early 2022 | ~$100M | $2B | $100M | 20x | Secondary round |

| Snyk | Dec 2021 | $230M | $8.4B | ~$150M | ~56x | Secondary within Series G |

| Kajabi | Nov 2021 | $550M | $2B | $100M | 20x | Minority PE investment |

| HighLevel (GoHighLevel) | Nov 2021 | $60M | ~$180M (est.) | ~$15M | ~12x | Minority recap |

| Lempire (Lemlist) | Nov 2021 | $30M | $150M | $10M | 15x | Minority recap |

| Zapier | Jan 2021 | ~$100M | $5B | $100M | 50x | Secondary recap |

| Calendly | Jan 2021 | $350M | $3B | ~$70M | 42.9x | Majority secondary |

| ISN (ISNetworld) | Dec 2020 | Minority investment | $2B+ | Undisclosed | — | Blackstone minority growth |

| Toast | Nov 2020 | Employee share sale | $8B | ~$120M (SaaS) | ~67x | Employee secondary (hybrid payments/SaaS) |

| Pipedrive | Nov 2020 | $150M | $1.5B | ~$90M | 16.7x | Majority recap |

| Supermetrics | Aug 2020 | ~$46M | $200M+ | ~$23M | ~10x | Series B + secondary |

| monday.com | May 2020 | Secondary share sale | $2.7B | ~$200M | ~13.5x | Investor secondary |

2010–2019 Era Transactions

| Company | Date | Secondary Liquidity | Valuation | ARR (Est.) | Rev. Multiple | Type |

|---|---|---|---|---|---|---|

| Kajabi | Nov 2019 | Minority growth | Undisclosed | ~$50M | — | Growth equity (Spectrum) |

| Wistia | Jul 2018 | $17.3M | ~$100M | ~$32M | 3.1x | Debt recap buyout |

| RFPIO | Jul 2018 | $25M | Undisclosed | ~$10–40M | — | Growth + secondary |

| SurveyMonkey | Jan 2013 | $800M | $1.35B | ~$180M | ~7.5x | Recapitalization |

| GitHub | Jul 2012 | $100M | $750M | ~$15M | ~50x | Series A (mostly secondary) |

| Qualtrics | 2012 | $70M | ~$350M (est.) | ~$50M | ~7x | Minority recap |

| iContact | Aug 2010 | $15M | $100M | $35M | ~2.9x | Growth + secondary |

| Atlassian | Jul 2010 | $60M | ~$400M | $59M | 6.8x | Minority recap |

| Squarespace | Jul 2010 | $38.5M | ~$80–100M | ~$9M | ~10x | Minority recap |

Note: Revenue multiples from the 2020–2021 period (20x–50x) reflect the peak of the SaaS valuation bubble. In 2024–2026, realistic multiples for most private SaaS companies range from 3x–8x revenue, depending on growth rate, profitability, and retention metrics.

While these 34 SaaS transactions show the range of what’s possible for traditional software companies, a new class of deals has emerged: AI-native software liquidity events. As we’ll explore in the next section, AI-native companies are commanding a 93% premium over SaaS multiples at secondary events (median 28x vs. 15x). Companies like Harvey AI (41x), Glean (36x), and Wiz (35x) are achieving revenue multiples that rival the 2021 SaaS bubble—but this time supported by 100%–300% annual growth rates rather than speculative exuberance.

Ready to Benchmark Your SaaS Metrics?

Join SaasRise to access benchmarking data, connect with peers who've done recap rounds, and get matched with the right investment banker for your ARR tier.

Apply to SaasRise →3. AI-Native Software: The New Wave of Founder Liquidity

The explosion of AI-native software companies since 2022 has created an entirely new category of founder liquidity events. Unlike traditional SaaS companies that added AI features over time, these companies were built from the ground up around artificial intelligence—and their rapid revenue growth has made them prime targets for secondary transactions, tender offers, and employee share sales.

What makes AI-native liquidity unique is the speed. Companies like Harvey AI went from founding to $100M ARR in roughly three years. ElevenLabs doubled its valuation between its Series C and tender offer in just nine months. Clay conducted two tender offers in under nine months, with valuations tripling from $1.5B to $5B. Decagon—less than three years old—completed its first employee tender offer at a $4.5B valuation in March 2026. Vercel ran a $300M tender at $9.3B alongside its Series F. This velocity means founders and early employees are accumulating paper wealth faster than ever—and the demand for structured liquidity is surging in response.

AI-Native Software Liquidity Rounds (2024–2026)

The following table captures confirmed secondary transactions, tender offers, and structured liquidity events at AI-native software companies (excluding frontier model companies like OpenAI and Anthropic, and hardware companies).

| Company | Date | Secondary Liquidity | Valuation | ARR (Est.) | Rev. Multiple | Type |

|---|---|---|---|---|---|---|

| Scale AI | May 2026 | Undisclosed | $25B | ~$2B | ~12.5x | Employee & investor tender offer |

| Decagon | Mar 2026 | Undisclosed | $4.5B | ~$30M+ | — | 1st employee tender offer (Coatue, a16z) |

| Clay | Jan 2026 | $55M | $5B | ~$120M | ~42x | 2nd employee tender offer (DST Global) |

| Synthesia | Jan 2026 | Undisclosed | $4B | ~$148M | ~27x | Employee tender offer |

| Harvey AI | Dec 2025 | Undisclosed | $8B | ~$195M | ~41x | First tender offer (alongside Series F) |

| Grammarly | 2025 | Undisclosed | ~$13B | ~$684M | ~19x | Secondary share sales |

| Vercel | Nov 2025 | $300M | $9.3B | Undisclosed | — | Employee & early investor tender offer (Accel, GIC) |

| Gong | Nov 2025 | Undisclosed | ~$4.5B | ~$300M | ~15x | Secondary round via Nasdaq Private Market |

| ElevenLabs | Sep 2025 | $100M | $6.6B | Undisclosed | — | Employee tender offer (Sequoia, ICONIQ) |

| Canva | Aug 2025 | Undisclosed | $42B | Undisclosed | — | Employee share sale (2nd tender) |

| Glean | Jun 2025 | Undisclosed | $7.2B | ~$200M | ~36x | Secondary market sales |

| Clay | May 2025 | Undisclosed | $1.5B | Undisclosed | — | 1st employee tender offer (Sequoia) |

| Linear | 2025 | Undisclosed | $1.25B | Undisclosed | — | Tender offer (matched Series C) |

| Runway ML | 2024–2025 | Secondary shares | ~$3B | ~$100M+ | ~30x | Secondary share sales (accredited investors) |

| Wiz | Sep 2024 | Undisclosed | ~$17.5B | ~$500M | ~35x | Tender offer (G Squared, Lightspeed) |

| Figma | May 2024 | $600–900M | $12.5B | Undisclosed | — | Shareholder tender offer |

Note: Excludes frontier model companies (OpenAI, Anthropic, Mistral, Cohere) and hardware/chip companies. Revenue multiples use ARR at time of transaction where available; estimated ARR is calculated from valuation ÷ revenue multiple where both are known. Canva and Figma also appear in the SaaS table above.

Key Patterns in AI-Native Liquidity

- Tender offers are the dominant structure: Unlike traditional SaaS minority recaps, AI companies overwhelmingly use company-facilitated tender offers rather than full secondary recapitalizations. This reflects both the speed of growth and the desire to retain control while providing employee liquidity.

- Repeat tenders are common: Clay conducted two tenders in nine months. Canva has done multiple share sales. This “rolling liquidity” model may become the standard for fast-growing AI companies.

- Valuations can move dramatically between events: ElevenLabs doubled its valuation in nine months. Clay tripled in nine months. Harvey went from $300M Series C (Jun 2025) to $8B Series F (Dec 2025) in six months. But corrections happen too—Gong’s secondary round valued the company at ~$4.5B, down from its $7.2B peak in 2021, even as ARR grew to $300M. The velocity of AI makes traditional 12–18 month fundraise cadences obsolete.

- Revenue multiples remain elevated: Where disclosed, AI-native companies command 12–41x revenue multiples in secondary transactions (median ~28x)—a 93% premium over the ~15x median for traditional SaaS at similar scale. Even Gong, whose valuation compressed from $7.2B to $4.5B, still achieved ~15x on $300M ARR—well above the broader private SaaS median of 4.1x.

- Employee retention is a primary driver: Many of these tenders are explicitly framed as retention tools. In a market where AI talent can earn $500K–$1M+ at competing companies, providing liquidity on paper wealth is essential for keeping teams intact.

What This Means for AI-Native Founders

If you are building an AI-native software company with strong revenue growth, the liquidity options available to you today are unprecedented. The key is reaching critical milestones:

- $10M+ ARR opens the door to structured secondary conversations

- $50M+ ARR with 100%+ growth makes tender offers highly viable

- $100M+ ARR creates demand from institutional secondary buyers and platforms like Forge, Nasdaq Private Market, and SecondaryLink

The AI wave has compressed the timeline from founding to meaningful liquidity from 7–10 years (typical for SaaS) down to 2–4 years. Founders who plan for structured liquidity early—setting up proper equity structures, 409A valuations, and investor relationships—will be best positioned to capture this opportunity.

Building an AI-Native Company?

SaasRise members include founders of leading AI software companies. Join to connect with peers who have navigated tender offers, secondary sales, and the unique challenges of AI company liquidity events.

Apply to SaasRise →4. Case Study: Ryan Allis & iContact

In August 2010, Ryan Allis was 25 years old and serving as CEO and co-founder of iContact, an email marketing SaaS platform that had grown to $35M in ARR with approximately 90% year-over-year revenue growth. After an “almost exit” to Salesforce fell through, Ryan and his team decided to pursue a different path: a minority recapitalization.

The iContact Minority Recap

- Date: August 2010

- Investor: JMI Equity (Baltimore-based growth equity firm)

- Total Round: $40M

- Primary Capital: $25M (into the company for growth)

- Secondary Capital: $15M (to buy shares from founders and early team)

- Valuation: $100M (~2.9x revenue multiple on $35M ARR)

- Shares Sold: Founders sold approximately 15% of their shares

- Founder Liquidity: Ryan personally took $3M off the table

- Subsequent Exit: Acquired by Vocus in February 2012 for $169M

The $3M in personal liquidity from the secondary round provided life-changing financial peace of mind at age 25, while still leaving the majority of Ryan’s equity intact for the larger exit that came 18 months later. The investment bank Allen & Co. ran the process and helped negotiate favorable terms.

Lesson: Ryan sold ~15% of his shares at a $100M valuation and took $3M off the table. The company later sold for $169M. By taking some chips off the table early, he locked in a win while preserving the vast majority of his upside for the bigger outcome. Most experienced entrepreneurs will tell you: if you get the chance to de-risk, do it.

How AI has changed the timeline: iContact reached $35M ARR in ~8 years before accessing its first liquidity event. Compare that to today’s AI-native companies: Harvey AI reached ~$195M ARR in roughly three years. Decagon went from founding to a $4.5B valuation with employee liquidity in under three years. Clay tripled its valuation from $1.5B to $5B in nine months. The fundamental lesson from iContact—take chips off the table when you can—applies equally to AI founders, but the window arrives far sooner. If you are building an AI-native company and growing at 200%+ annually, the liquidity conversation should start at $10M ARR, not $35M.

5. The State of the Secondary Market in 2025–2026

Before we dive in, let’s be clear about what “the secondary market” actually means. When a company raises money from investors, that’s the primary market—new shares are created and sold. The secondary market is when existing shareholders (founders, employees, early investors) sell shares they already own to new buyers. It’s the same concept as a stock exchange, but for private companies.

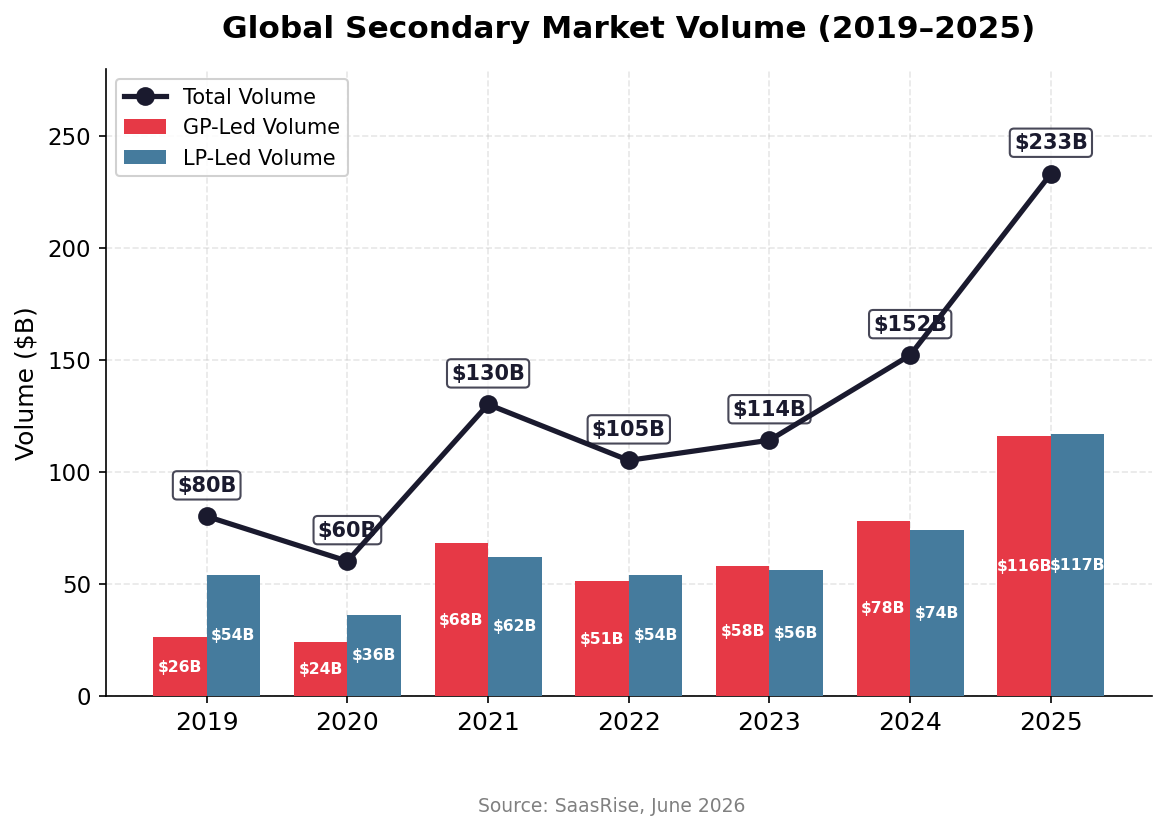

This market has undergone a massive transformation. What was once a niche corner of private equity has become a mainstream $233 billion market—and it’s the engine that makes founder liquidity possible without an IPO or company sale.

Record Volume in 2025

According to Lazard’s 2025 Secondary Market Report, estimated aggregate secondary deal volume reached approximately $233 billion in 2025, a 53% increase over 2024. This growth was driven by two engines: investors selling their fund stakes (LP-led deals) and fund managers creating structured liquidity events (GP-led deals), which accounted for roughly 50% of total market volume.

The Rise of GP-Led Transactions

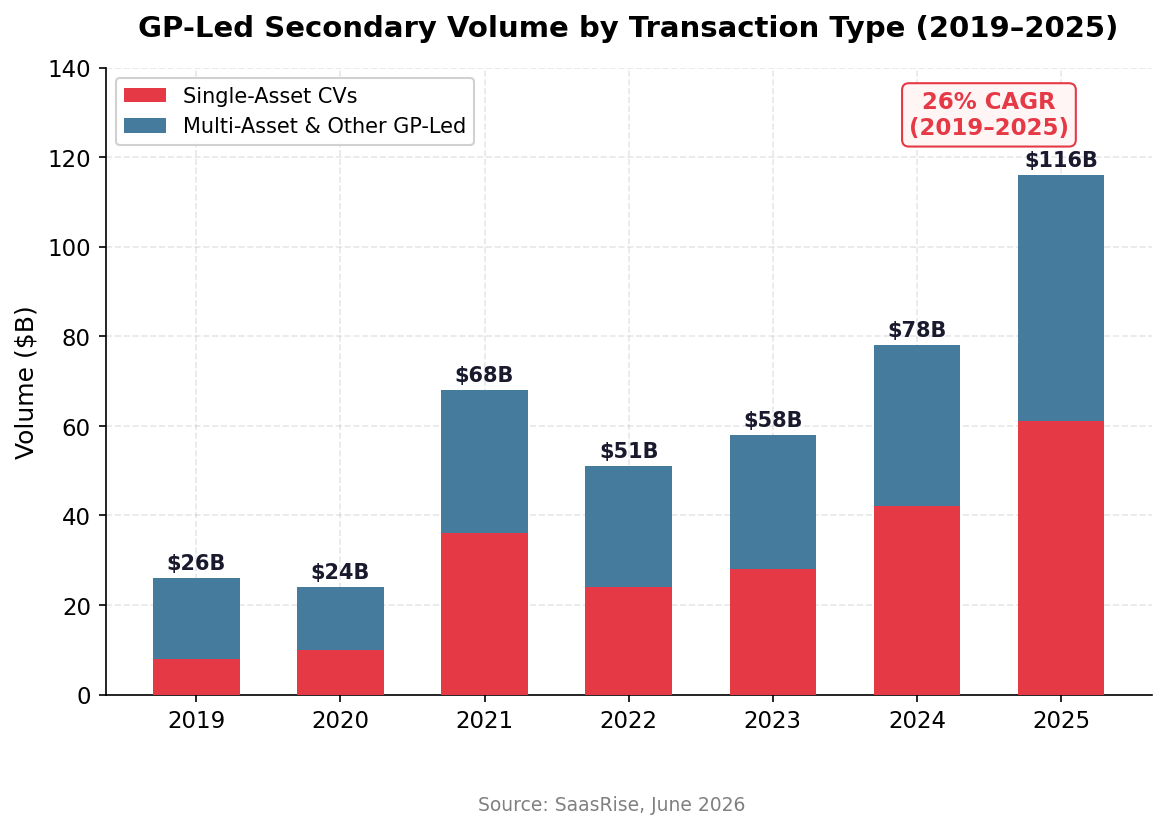

GP-led secondary transactions—including continuation vehicles, tender offers, and structured liquidity programs—have emerged as the fastest-growing segment of the secondary market. Total GP-led volume reached $116 billion in 2025, exhibiting a 26% compound annual growth rate since 2019.

📚 Jargon Buster: What Are “GP-Led” and “LP-Led” Deals?

The secondary market has two main types of deals, and the names come from the world of private equity funds:

• LPs (Limited Partners) are the investors who put money into a PE or VC fund—think pension funds, university endowments, wealthy families. An LP-led deal is when one of these investors decides to sell their stake in a fund to someone else. It’s like selling your seat at a poker table to another player mid-game.

• GPs (General Partners) are the fund managers who actually pick and manage the companies—firms like Insight Partners, Vista Equity, or Sequoia. A GP-led deal is when the fund manager itself orchestrates a liquidity event. The most common version is a continuation vehicle: instead of selling a company, the GP moves it into a new fund, giving existing investors the choice to cash out or stay in. Think of it as the fund manager saying: “This company is doing so well that we don’t want to sell it yet—but we’ll give you the option to take your money off the table.”

Why does this matter to you as a founder? GP-led deals—especially tender offers and continuation vehicles—are now the fastest-growing part of the secondary market, and they’re the mechanism that creates liquidity for founders and employees. When we say “GP-led volume hit $116B,” what we really mean is: fund managers are creating more opportunities for people like you to sell shares without a full company sale.

Within GP-led transactions, single-asset continuation vehicles have been the standout performer, growing at a 48% CAGR since 2019 and representing approximately 53% of total GP-led volume in 2025. Technology remained the most active sector for single-asset continuation funds, accounting for roughly 27% of deal flow, as investors were drawn to recurring SaaS revenue models, strong growth and margin profiles, and the consistent earnings performance of more mature software companies.

Key Market Dynamics

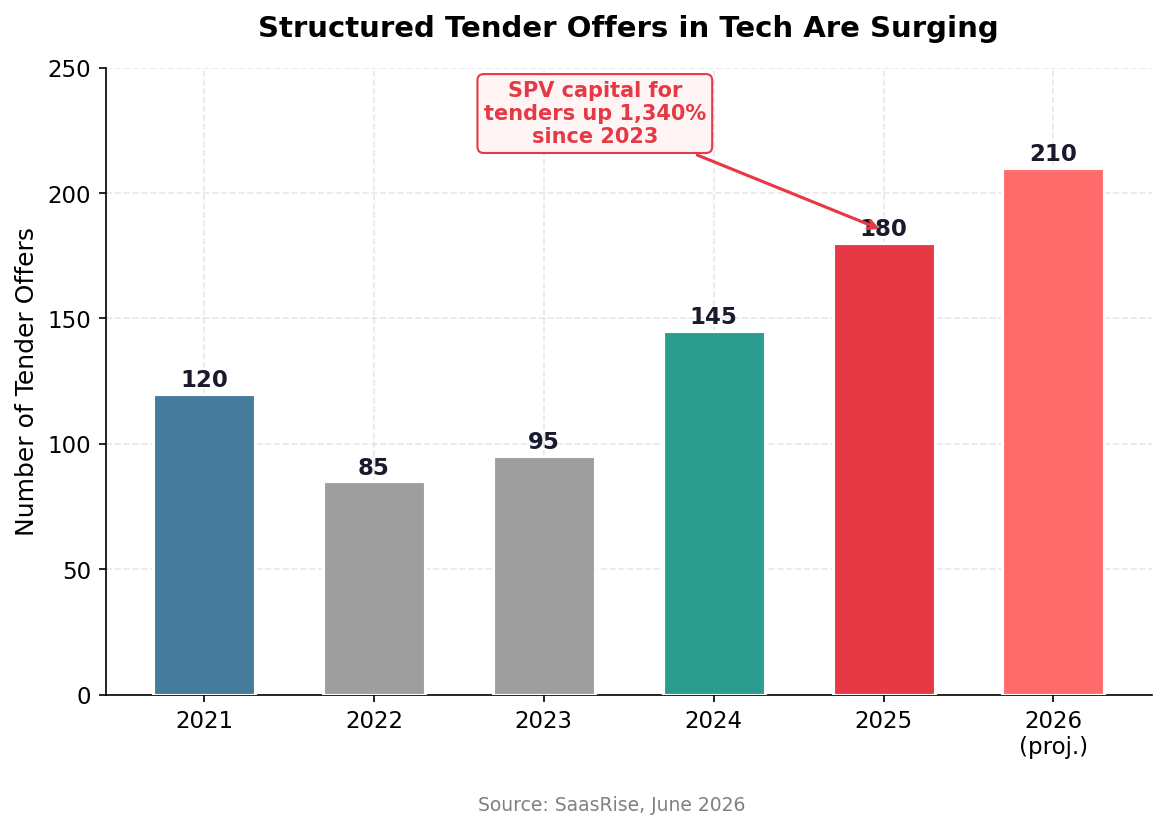

- More sellers than buyers: There’s so much demand to sell secondary shares that buyers can barely keep up. The ratio of available buyer capital to seller volume is near all-time lows at 1.0x—meaning for every dollar someone wants to sell, there’s roughly one dollar of buyer capital available. This is good news for you as a founder: buyer competition keeps pricing healthy.

- Tender offers surging: Tender offer deal count reached its highest level since 2022, with secondary SPV capital raised for tenders jumping 1,340% since 2023. AI-native software companies have been a major driver of this surge—Harvey AI, Scale AI, Vercel, ElevenLabs, Clay, and Decagon all ran structured tenders in 2025–2026, with Vercel’s $300M tender and Scale AI’s at $25B among the largest.

- AI-native companies are accelerating the trend: The speed at which AI software companies reach scale—Harvey AI went from founding to ~$195M ARR in three years; Decagon hit $4.5B valuation in under three years—means founders and employees are accumulating paper wealth faster than ever, creating unprecedented demand for structured liquidity.

- This isn’t going away: 100% of secondary market investors surveyed by DC Advisory expect this market to keep growing over the next 2–3 years. 60% expect significant growth. This is now a permanent feature of how private companies provide liquidity.

- Not a sign of desperation: 90% of fund managers say secondary transactions are a healthy complement to traditional exits (acquisitions or IPOs)—not a sign that something is wrong. Running a tender offer or secondary sale is increasingly seen as smart financial management, not a red flag.