The AI Software Valuation Report 2026

This report compares venture capital investment multiples and M&A revenue multiples across three categories of software companies in Q1 2026: AI-Native Software (companies built entirely around AI from inception), AI-Enabled Software (established platforms with meaningful AI integration), and Legacy SaaS (traditional per-seat subscription businesses without significant AI). Using data from Finro, Windsor Drake, Aventis Advisors, PitchBook, Software Equity Group, and other industry sources covering 575+ AI companies and 620+ M&A transactions, we quantify the growing valuation gap between these three tiers.

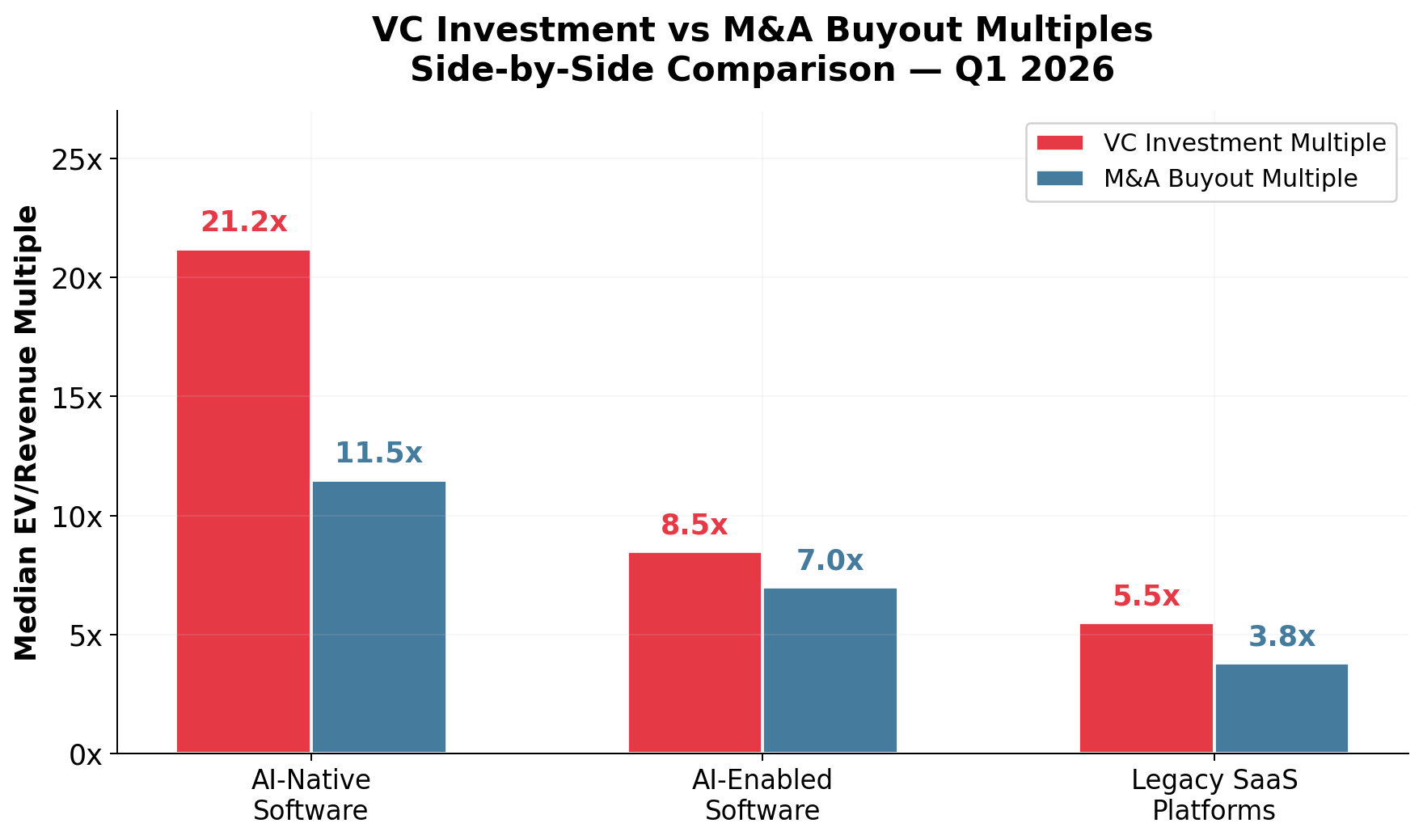

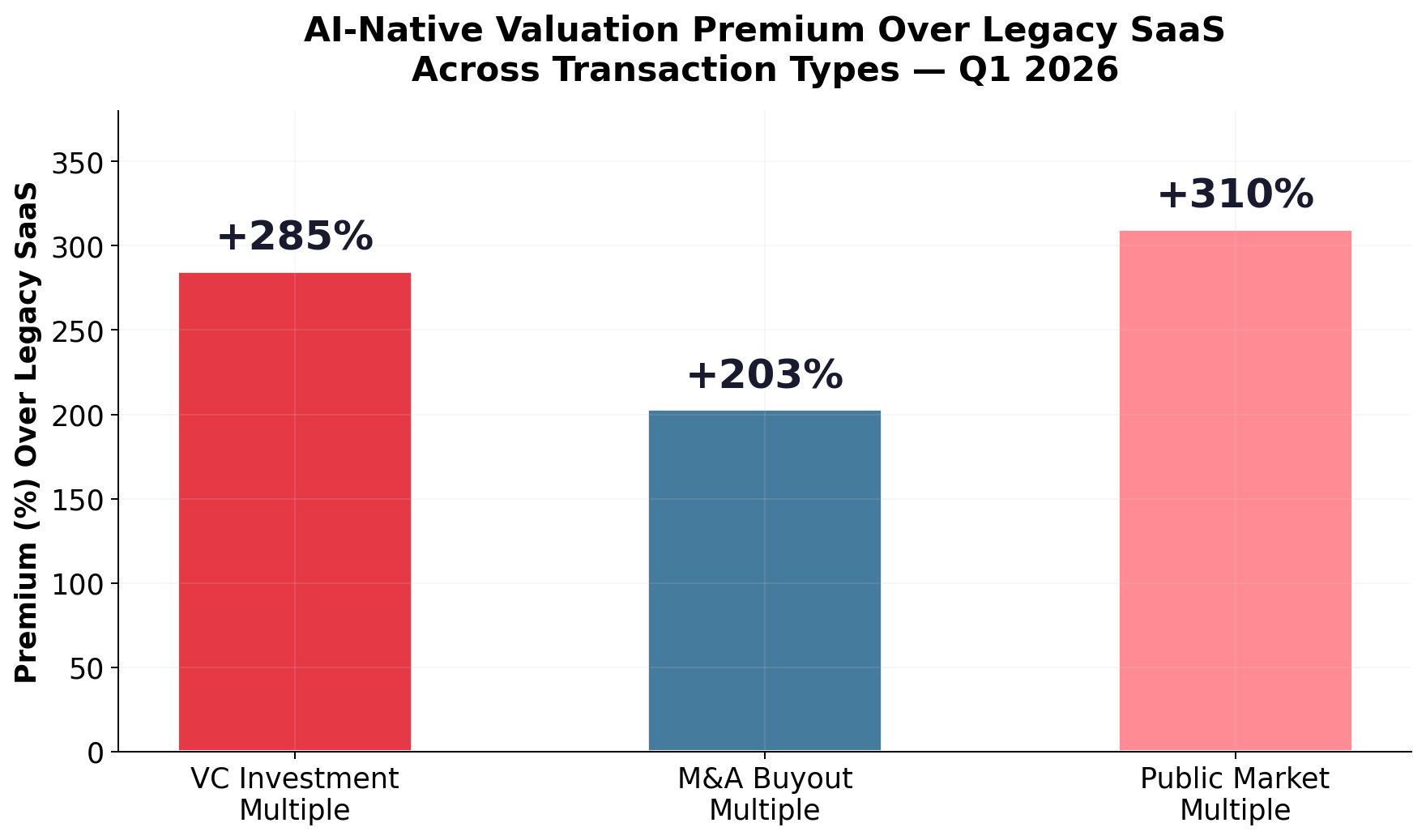

The findings are striking. AI-native companies command a median 21.2x EV/Revenue in VC rounds and 11.5x in M&A buyouts, compared to just 5.5x (VC) and 3.8x (M&A) for legacy SaaS — a premium of 200–285%. This report breaks down the data, profiles mid-market case studies in the $1M–$100M ARR range, and provides a framework for understanding where AI software valuations are headed.

This report is published by SaasRise, the #1 mastermind community for SaaS CEOs with $1M–$100M+ in ARR. Members have collectively raised $1B+ and have $3B+ in ARR.

VC Deal Multiples (Minority Investment Rounds)

M&A Deal Multiples (Buyout Transactions)

Why are M&A multiples lower than VC multiples? Venture capital investments are typically made earlier in a company’s lifecycle when growth rates are highest and revenue bases are smaller, so investors pay a premium for future potential. M&A buyouts, by contrast, occur later — when companies have larger revenue bases, slower growth, and acquirers are pricing current cash flows rather than speculative upside. The result: M&A revenue multiples are structurally lower, but they represent realized exit values rather than paper valuations.

📋 Table of Contents

- Defining the Three Categories

- Venture Capital Investment Revenue Multiples

- M&A Revenue Multiples (Buyout Transactions)

- VC vs M&A Multiples — Side-by-Side Comparison

- The SaaSpocalypse — Legacy SaaS Under Pressure

- Mid-Market Case Studies ($1M–$100M ARR)

- The Widening Gap — Historical Trajectory

- The AI Integration Valuation Framework

- The Coming AI IPO Wave

- Conclusion: The Data is Unambiguous

- Sources & References

This report examines the growing valuation divergence across three categories of software companies: AI-Native Software, AI-Enabled Software, and Legacy SaaS Platforms. Using Q1 2026 and April 2026 data from Finro, Windsor Drake, Aventis Advisors, PitchBook, Software Equity Group, Berkery Noyes, and other industry sources, we quantify the AI valuation premium across both venture capital investment rounds (where investors take minority stakes at growth-stage valuations) and M&A transactions (where acquirers purchase majority or full ownership at buyout valuations).

The data supports a clear hypothesis: companies that are AI-native consistently receive higher revenue multiples in both VC investment rounds and M&A buyout transactions, and this premium is accelerating in 2026.

1. Defining the Three Categories

Not all software companies are valued equally. As AI reshapes the technology landscape, investors and acquirers are increasingly segmenting the software market into three distinct tiers, each commanding fundamentally different valuation multiples.

1. AI-Native Software Companies

Definition: Companies whose core product is built entirely around artificial intelligence. AI is not a feature — it is the product. These companies develop proprietary models, leverage unique training data, and deliver value through autonomous AI workflows.

Examples: OpenAI ($300B valuation, 81.1x EV/Revenue), Anthropic ($61.5B, 70.3x), Cursor ($50B), Harvey (legal AI, $11B), ElevenLabs (voice AI, $11B), Perplexity (AI search, $20B), Synthesia (AI video, $4B).

Key Characteristics: Proprietary AI models or unique data moats; consumption-based pricing; AI agents replacing human workflows; NRR often exceeding 135%; exponential revenue growth (many growing 100%+ YoY).

2. AI-Enabled Software Companies

Definition: Established software companies that have meaningfully integrated AI capabilities into existing products, creating measurable value through AI-powered features, automation, and intelligence layers.

Examples: Palantir (20.3x EV/Revenue), CrowdStrike, Datadog, ServiceNow, Palo Alto Networks, Salesforce (Agentforce, $800M ARR), Snowflake, Databricks ($5.4B ARR, 140% NRR).

Key Characteristics: Meaningful AI integration (not just a wrapper); AI drives measurable customer ROI; hybrid pricing (per-seat + consumption); strong retention; typically 15-40% revenue growth.

3. Legacy SaaS Platforms (No Meaningful AI)

Definition: Traditional SaaS companies relying primarily on per-seat subscription models without meaningful AI integration. They face the greatest disruption risk as AI-native alternatives emerge.

Examples: Many horizontal point-solution SaaS companies in CRM, project management, HR, document management; products where one AI agent can replace 5+ seats.

Key Characteristics: Per-seat subscription pricing; revenue growth below 10-12%; limited AI integration; high vulnerability to AI substitution; shrinking TAM as AI agents reduce seat count.

2. Venture Capital Investment Revenue Multiples

VC investment multiples measure the enterprise value (EV) divided by revenue at the time of a minority venture investment round. These are not buyout prices — they reflect what investors pay for a minority stake, typically at Series A through Series D+. Because VC investors price future potential rather than current cash flows, these multiples tend to be significantly higher than M&A transaction multiples.

The AI-Native Premium in VC Rounds

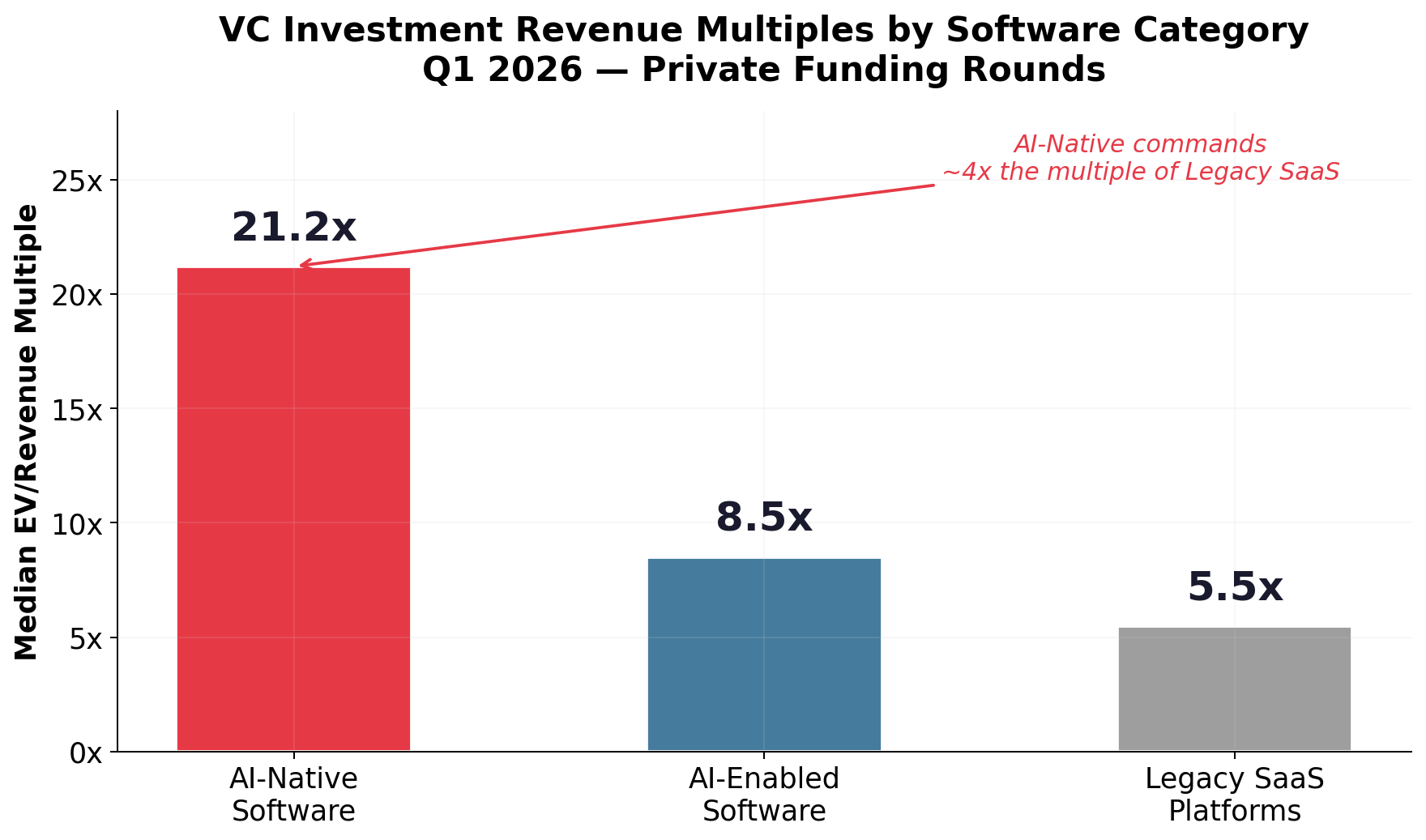

According to Finro’s Q1 2026 dataset covering 575 AI companies, the median VC investment multiple for AI infrastructure was 21.2x EV/Revenue, with 39.5x for LLM vendors and 36.9x for AI search engines.

Windsor Drake’s Q1 2026 SaaS Valuation Report shows private SaaS venture multiples ranging from 4.8x (bootstrapped) to 5.3x (equity-backed). AI-native platforms command 16x to 18x — a 40-80% premium over the next tier.

Aventis Advisors found a median of 29.7x across AI fundraising rounds vs. ~6x for public SaaS. Eqvista’s Q1 2026 research confirmed AI companies average 37.5x vs. just 7.6x for SaaS. Eqvista’s fundraising data shows seed-stage AI startups receive valuations approximately 42% higher than non-AI peers.

Key Insight — VC Investment Multiples: AI-native companies command a median 21.2x EV/Revenue in venture rounds, roughly 4x the 5.5x median for legacy SaaS. The range is enormous — from 10x for applied AI to 75x+ for LLM vendors. AI-enabled companies sit at approximately 8.5x, earning a meaningful premium over legacy SaaS but far below the AI-native stratosphere.

VC Multiples by AI Niche

Finro’s dataset reveals dramatic dispersion across 15 AI niches. The highest multiples accrue to foundational “picks and shovels” — LLM Vendors (73.5x average), AI search engines (40.7x), and infrastructure providers (31.3x). Applied AI in specific verticals trades at lower but substantial premiums: Health Tech (23.8x), Marketing Tech (30.3x), and Cybersecurity (21.5x).

The Finro Q1 2026 Update highlights: Core AI and Applied AI did not converge — the gap widened. Investors increasingly price commercialization certainty rather than technical sophistication.

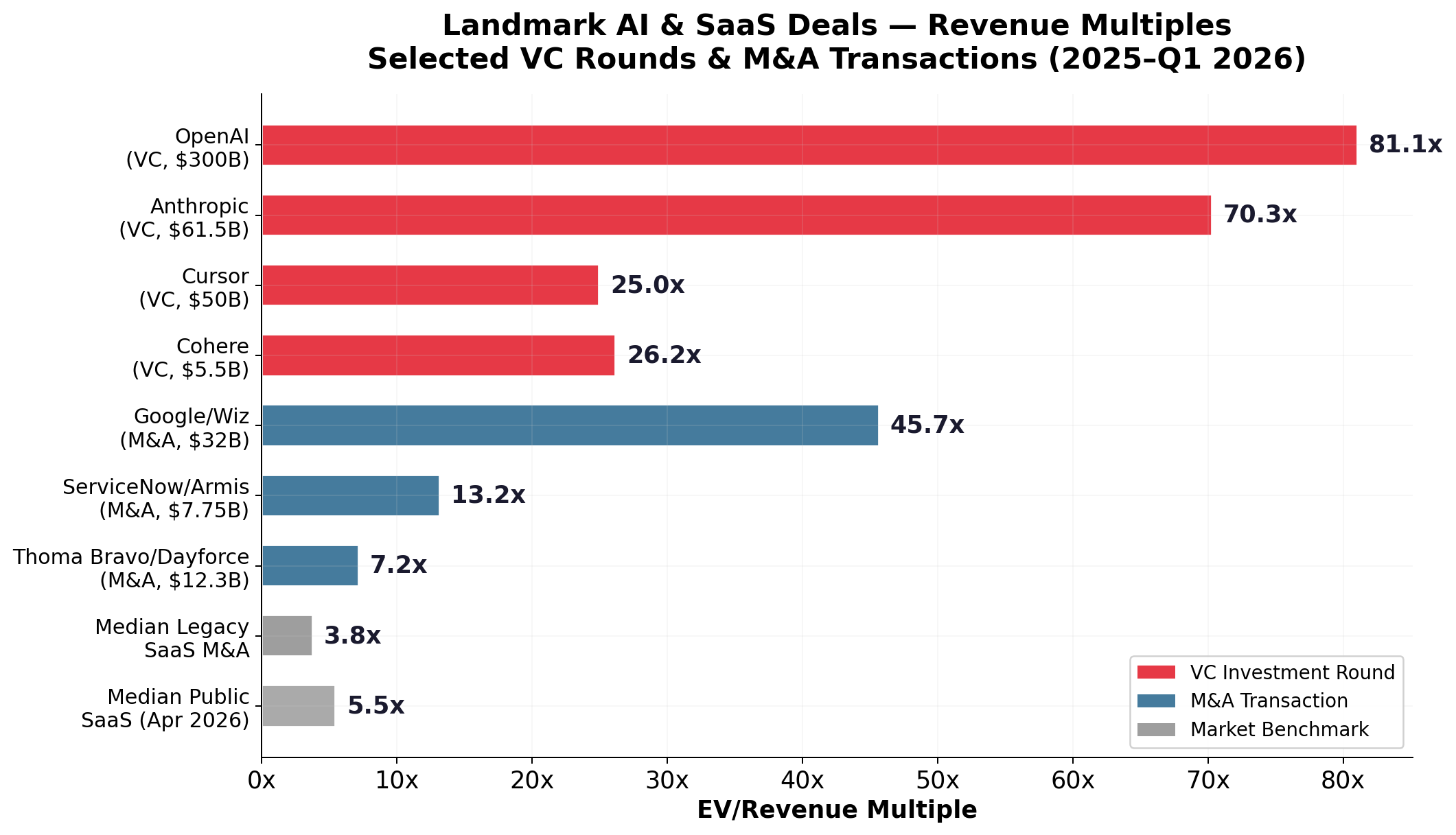

Landmark VC Rounds: The Numbers Behind the Headlines

| Company | Category | Valuation | Revenue | EV/Revenue | Type |

|---|---|---|---|---|---|

| OpenAI | AI-Native (LLM) | $300B | $3.7B | 81.1x | VC Round |

| Anthropic | AI-Native (LLM) | $61.5B | $875M | 70.3x | VC Round |

| Cursor | AI-Native (Dev Tools) | $50B | $2B ARR | ~25x | VC Round |

| Perplexity | AI-Native (Search) | $20B | $500M ARR | 40x | VC Round |

| Scale AI | AI-Native (Data) | $13.8B | $870M | 15.9x | VC Round |

| ElevenLabs | AI-Native (Voice) | $11B | $330M ARR | 33.3x | Series D |

| Harvey | AI-Native (Legal) | $11B | $100M+ ARR | ~100x | Series F |

| Cohere | AI-Native (LLM) | $5.5B | $210M | 26.2x | VC Round |

| Databricks | AI-Enabled | $135B | $5.4B ARR | ~25x | Pre-IPO |

| Palantir | AI-Enabled | $58.4B | $2.87B | 20.3x | Public |

Sources: Finro Q1 2026; TechCrunch; ElevenLabs Blog; Sacra.

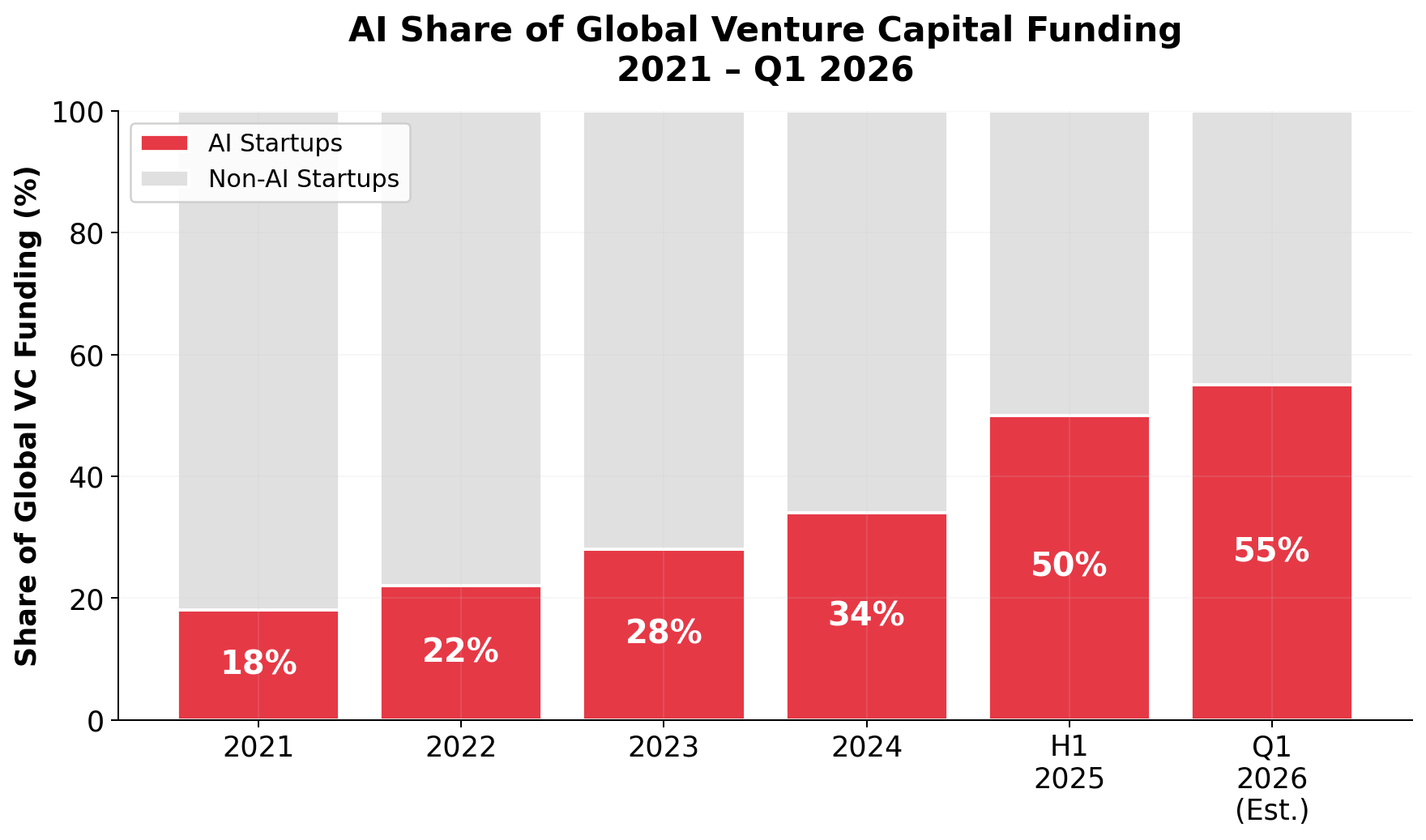

In 2025, approximately 50% of all global VC dollars went into AI startups, up from 34% in 2024 (Eqvista). CB Insights reported 266 AI M&A deals in Q1 2026 alone, a 90% increase year-over-year (FE International).

3. M&A Revenue Multiples (Buyout Transactions)

M&A revenue multiples measure the enterprise value at which a company is acquired — typically in a majority sale or full buyout. These differ fundamentally from VC investment multiples because the buyer is purchasing control and assuming operational risk. M&A multiples are typically lower than VC multiples but represent real “exit” values.

The Three-Tier M&A Landscape

Q1 2026 saw an estimated 620+ SaaS-specific M&A transactions worth over $95 billion in aggregate deal value, headlined by Google’s $32B acquisition of Wiz, Palo Alto Networks’ $25B purchase of CyberArk, and Thoma Bravo’s $12.3B take-private of Dayforce (SaasRise Q1 2026 Report).

FE International’s April 2026 analysis confirmed that AI-native companies command M&A revenue multiples of 8x to 15x, with outliers exceeding 20x for businesses with proprietary data assets and NRR above 120%.

M&A Multiples by Segment

| Segment | Category | M&A EV/Revenue | Premium vs Avg |

|---|---|---|---|

| AI Infrastructure | AI-Native | 14.5x – 15.0x | +175% |

| AI-Native SaaS | AI-Native | 9.5x – 14.0x | +75% |

| Cybersecurity (AI) | AI-Enabled | ~11.0x | +107% |

| Healthcare IT (AI) | AI-Enabled | ~9.0x | +70% |

| Vertical SaaS + Finance | AI-Enabled | 7.0x – 9.5x | +32-79% |

| Traditional SaaS (Avg) | Legacy SaaS | 5.3x – 5.4x | Baseline |

| Median Private SaaS M&A | Legacy SaaS | 3.8x | Below baseline |

Sources: Windsor Drake M&A Q1 2026; SaasRise Research.

Mega-Deal Case Studies

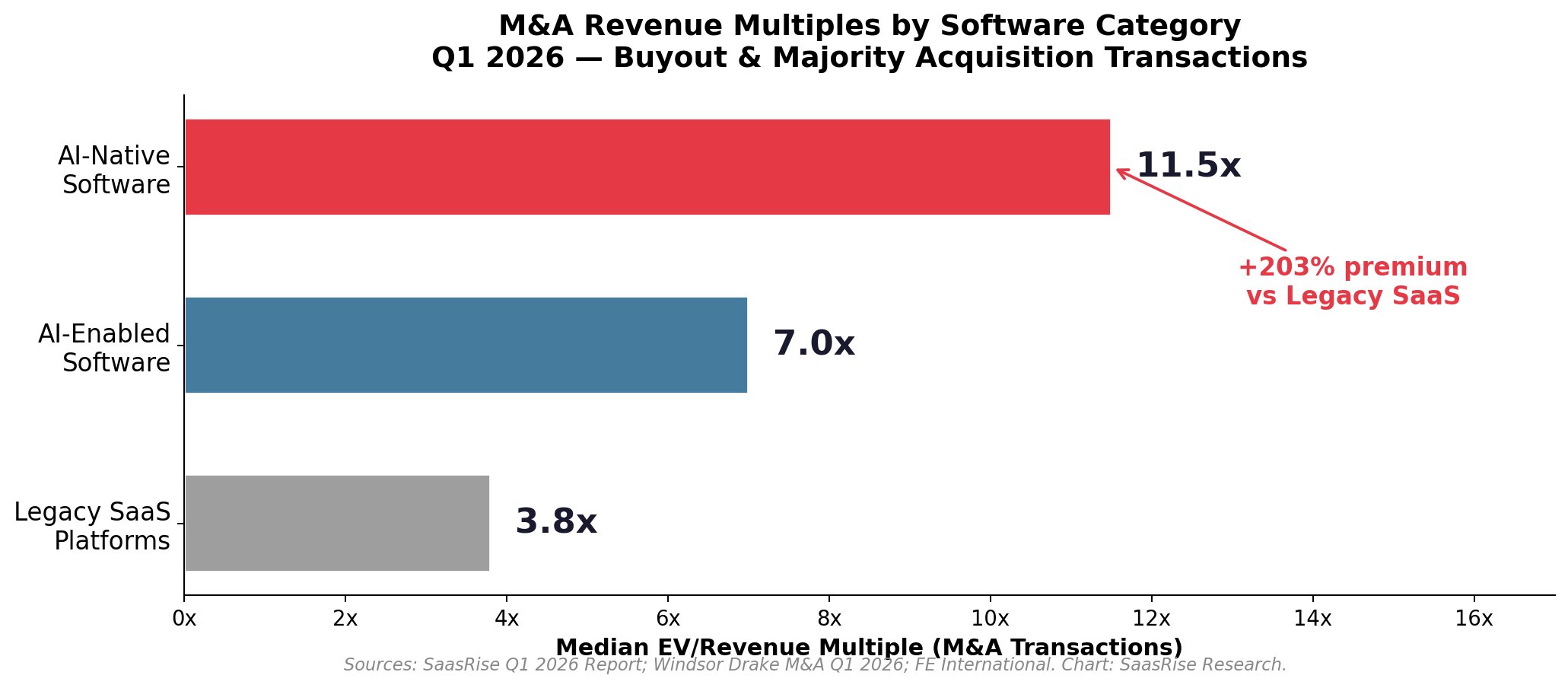

Key Insight — M&A Multiples: In private M&A, AI-native companies sell for a median of approximately 11.5x revenue (with top-quartile assets reaching 14x+), compared to just 3.8x for median private SaaS. Buyers pay more per dollar of revenue for AI-native capabilities because these companies grow faster, retain customers more effectively, and are more defensible long term.

4. VC vs M&A Multiples — Side-by-Side Comparison

One of the most important distinctions is between VC investment multiples and M&A revenue multiples. These are fundamentally different transaction types.

VC Investment Multiples (Minority Stakes)

Higher because investors price future potential — buying a minority stake in a company they believe will grow 10x+ over 5-7 years.

M&A Revenue Multiples (Buyout Transactions)

Lower because buyers purchase control — assuming operational risk, integration complexity, and the obligation to realize near-term value.

The data reveals a consistent pattern: the AI premium exists in both VC and M&A transactions, but is amplified in VC rounds. AI-native companies trade at approximately 1.8x their M&A value in VC rounds (21.2x vs 11.5x).

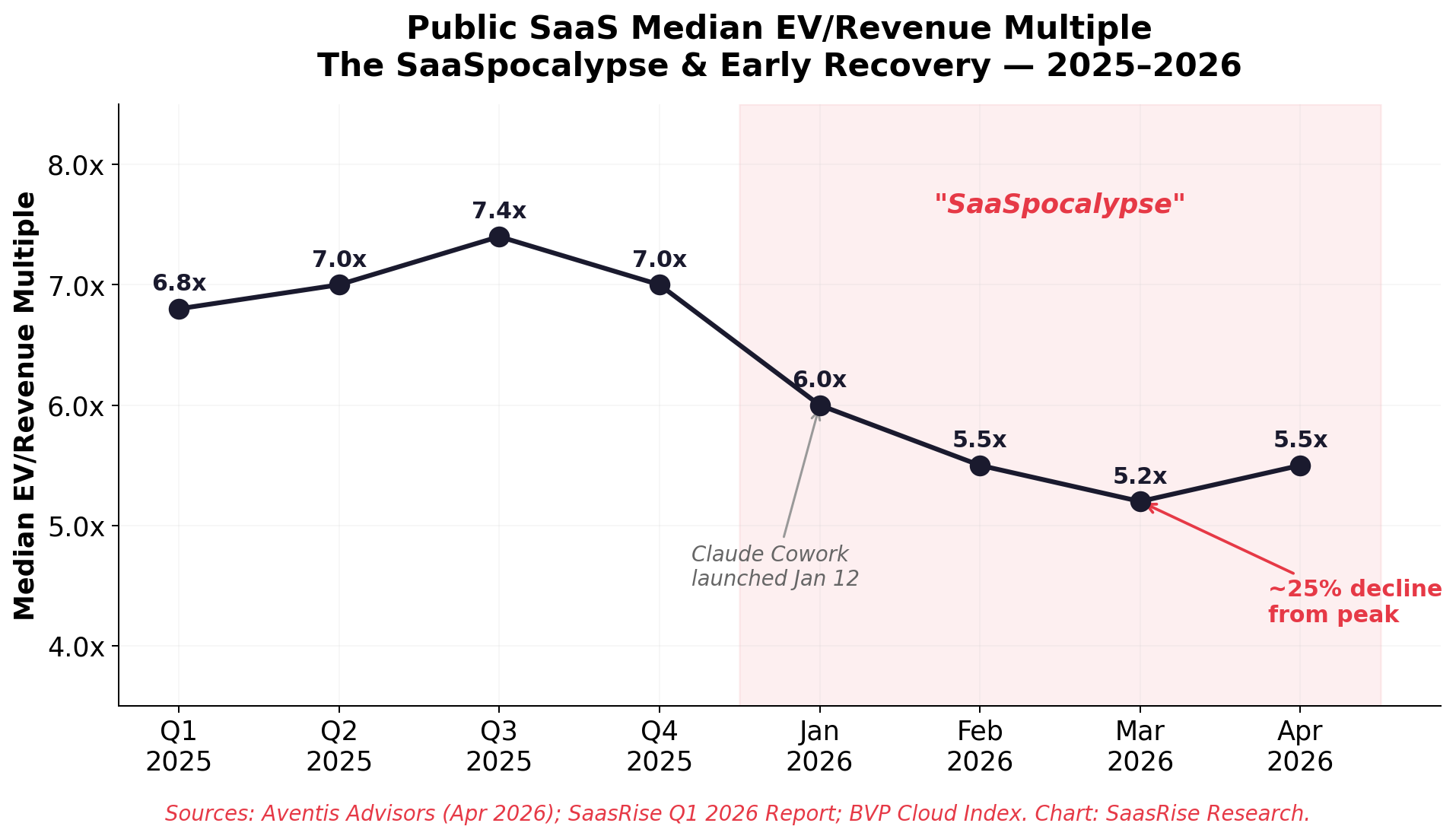

5. The SaaSpocalypse — Legacy SaaS Under Pressure

On January 12, 2026, Anthropic launched Claude Cowork — an autonomous AI agent capable of performing end-to-end business workflows (Taskade). Approximately $2 trillion in market cap was erased within weeks (Digital Applied). Public SaaS median EV/Revenue declined from ~7.0x to approximately 5.2x by March 2026 — a roughly 25% compression from peak — before recovering to ~5.5x by April (SaasRise Q1 2026 Report; BVP Cloud Index).

The hardest-hit stocks were overwhelmingly legacy SaaS platforms:

| Company | Category | YTD Decline | Market Signal |

|---|---|---|---|

| Atlassian | Legacy SaaS | -35% | First-ever negative enterprise seat growth |

| Salesforce | AI-Enabled | -28% | Net-new customer acquisition slowing |

| HubSpot | Legacy/AI-Enabled | -25% | SMB churn to AI-native CRMs |

| ServiceNow | AI-Enabled | -22% | AI agent competition in ITSM |

| IGV ETF | Benchmark | -22% | Sector entered technical bear market |

| Workday | Legacy SaaS | -20% | HR automation concerns; announced layoffs |

| Zendesk | Legacy SaaS | -18% | AI handling 80%+ of tier-1 support tickets |

Sources: Digital Applied; Taskade; MarketMinute.

The structural driver: 40% of IT budgets are being reallocated from legacy SaaS toward agentic platforms and LLM token usage (MarketMinute). Per-seat pricing adoption dropped from 21% to 15% of enterprise contracts in 12 months (Taskade).

6. Mid-Market Case Studies ($1M–$100M ARR)

While mega-deals like OpenAI ($300B) and Google/Wiz ($32B) capture headlines, the AI valuation premium is equally pronounced in the $20M to $500M fundraise range that most growth-stage SaaS companies compete in. Below are detailed case studies for companies in the $1M to $100M+ ARR range at the time of their most relevant transaction.

AI-Native: $1M–$100M ARR Range

ElevenLabs (Voice AI)

Raised $500M led by Sequoia. Voice AI platform with enterprise clients including Deutsche Telekom, Revolut, and SAP. ARR grew from near-zero to $330M in ~24 months. Tripled valuation in 12 months.

Harvey (Legal AI)

Raised at $11B, up from $8B just 4 months earlier and $3B one year prior. Serves 50+ AmLaw 100 firms. Investors include a16z, Sequoia, Kleiner Perkins.

Synthesia (AI Video)

Raised $200M led by GV. AI video for corporate training. Enterprise clients include Bosch, Merck, SAP. Hit $100M ARR in April 2025. Nearly doubled valuation from $2.1B.

Glean (Enterprise AI Search)

Raised $150M. Enterprise AI search platform. Doubled ARR from $100M to $200M+ in 9 months. Powers knowledge discovery for enterprises globally.

Codeium/Windsurf (AI Coding)

Led by Kleiner Perkins. AI coding assistant competing with Cursor. Launched Windsurf Editor with agentic coding. At $40M ARR, achieved a 71x revenue multiple.

Runway ML (AI Video Generation)

Raised $315M. Creative AI platform with Gen-3 video models. Revenue growing ~140% YoY. Consumer + enterprise mix.

Lovable (AI App Builder)

Led by CapitalG and Menlo Ventures. 25M+ total projects in first year. Strategic investors: NVIDIA, Salesforce, Databricks, Atlassian, HubSpot.

Jasper AI (Content Generation)

AI content platform with 1.8M+ monthly users across 120+ countries. Shows how multiples vary: Jasper at ~10x (wrapper perception) vs. proprietary model companies at 30-70x+.

Key Pattern — Mid-Market AI-Native: Even at the $40M-$330M ARR range, AI-native companies consistently command 30x-70x EV/Revenue. The premium is highest for companies with proprietary models (Harvey at ~100x, Codeium at ~71x) and lower for companies perceived as API wrappers (Jasper at ~10x). This confirms the Windsor Drake finding that “authenticity matters.”

AI-Enabled Mid-Market: Transition Premium

AI-enabled companies in the $1M-$100M ARR range command a meaningful but smaller premium. Windsor Drake’s framework shows these companies typically trade at 7.5x to 14.0x:

Legacy SaaS Mid-Market: Compression Accelerating

For legacy SaaS in the $1M-$100M ARR range without meaningful AI, the multiple environment has deteriorated. Aventis Advisors reports median private SaaS M&A multiple fell to 3.1x as of March 2026 (from 3.8x in 2025), bottom quartile below 2.0x. Deal size matters: median revenue multiples are nearly twice as high for $50-100M deals vs. $20-50M deals.

| ARR Range | AI-Native Multiple | AI-Enabled Multiple | Legacy SaaS Multiple |

|---|---|---|---|

| $1M – $5M | 15x – 30x | 6x – 9x | 2.5x – 4.0x |

| $5M – $20M | 20x – 40x | 7x – 12x | 3.0x – 5.0x |

| $20M – $50M | 25x – 50x | 8x – 14x | 3.5x – 6.0x |

| $50M – $100M | 30x – 70x | 10x – 16x | 4.0x – 7.0x |

Note: Ranges are composite estimates based on Finro Q1 2026, Windsor Drake Q1 2026, Aventis Advisors, Eqvista, and case study data cited in this report.

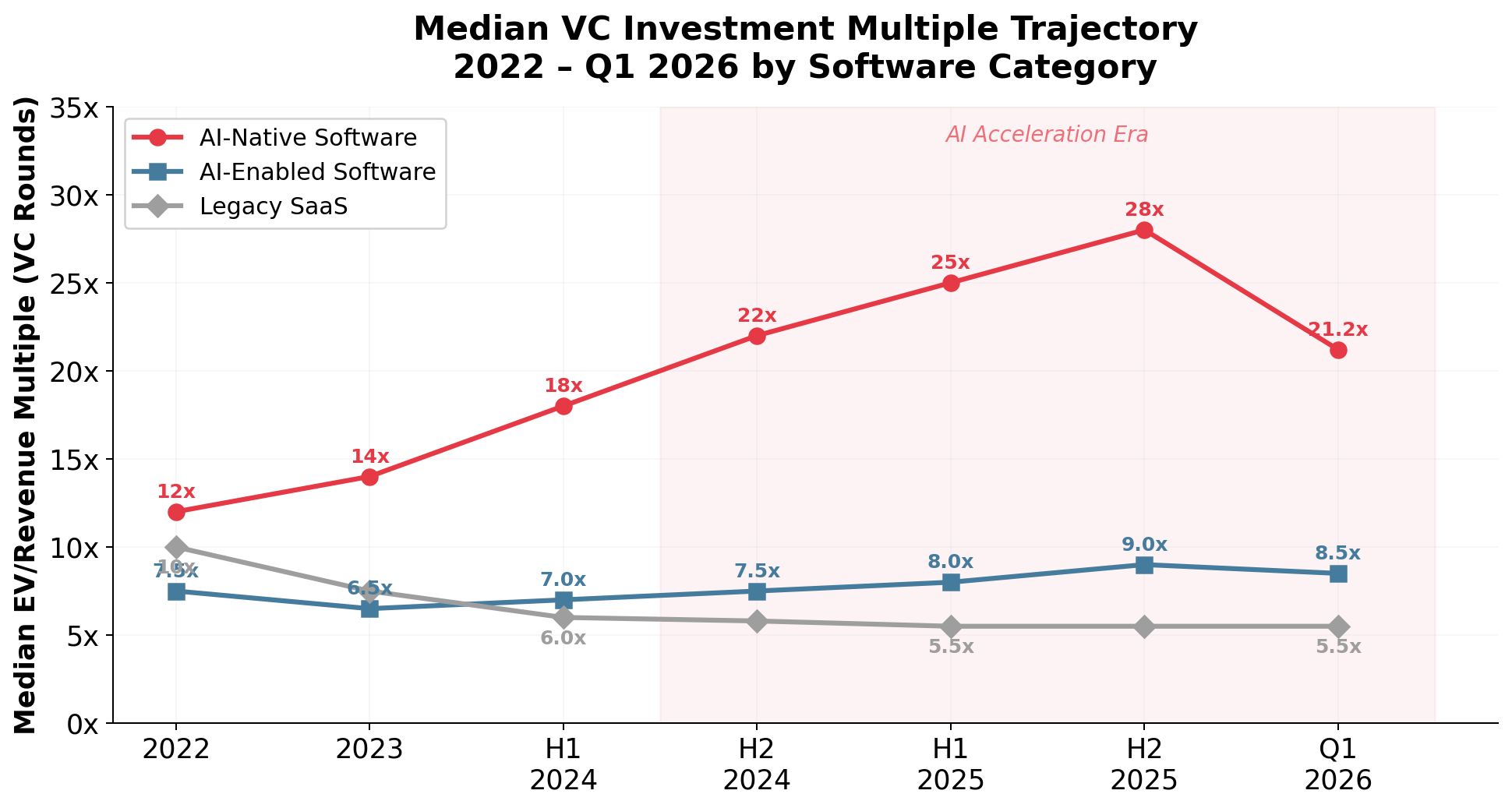

7. The Widening Gap — Historical Trajectory

The AI valuation premium has accelerated dramatically since 2024. Tracing median VC investment multiples reveals a clear divergence:

- AI-Native multiples surged in 2024-2025 as foundational AI companies demonstrated rapid revenue growth, pushing multiples from ~18x to ~28x.

- Legacy SaaS multiples compressed as sector revenue growth slowed from 17% (Q4 2023) to 12.2% (Q4 2025).

- AI-Enabled carved out a middle tier as investors rewarded meaningful AI integration but penalized superficial efforts.

- Q1 2026 correction brought AI-native multiples down slightly from their H2 2025 peak, but the gap vs legacy widened because legacy fell further.

The Efficiency Equation: Rule of 40 and AI

Aventis Advisors data shows each 10-point Rule of 40 improvement linked to a 1.1x increase in EV/Revenue. Crucially, AI-native companies earn higher multiples at every Rule of 40 level compared to legacy SaaS — confirming the premium is structural, not simply a function of higher growth rates.

8. The AI Integration Valuation Framework

Windsor Drake’s Q1 2026 Report introduced a framework quantifying valuation premiums by depth of AI integration:

| AI Integration Level | Our Category | EV/Revenue Range | Premium vs Baseline |

|---|---|---|---|

| AI-Native Platform | AI-Native Software | 16.0x – 18.0x | +40 – 80% |

| Deep AI Integration | AI-Enabled (High) | 9.5x – 14.0x | +40 – 60% |

| Moderate AI Features | AI-Enabled (Low) | 7.5x – 9.5x | +20 – 35% |

| AI Roadmap Only | Legacy (Transitioning) | 6.0x – 7.5x | +5 – 15% |

| No AI Strategy | Legacy SaaS | 5.5x – 7.0x | Baseline |

Source: Windsor Drake SaaS Valuation Report Q1 2026.

Windsor Drake emphasizes that “authenticity matters” — investors distinguish genuine AI value from “AI washing.” Proprietary AI commands higher premiums than third-party API wrappers.

9. The Coming AI IPO Wave

The ultimate test of AI-native valuation premiums will come with the expected IPOs of OpenAI, Anthropic, and Databricks in 2026 — carrying combined last-round valuations approaching $1.4 trillion (Morningstar/PitchBook).